Prudential Regulatory Authority (PRA)

In the perspective of financial regulation, prudential regulatory reporting is the process by which financial, specifically banks and insurers, submit elaborated financial data to regulatory authorities (e.g., Prudential Regulatory Authority, UK) regarding their financial health, practices of risk management, and operational activities.

By submitting the PRA report, financial institutions demonstrate their compliance with the rules entrenched to guarantee financial stability and prevention of systemic risk. In essence, it is a mechanism through which institutions demonstrate that they are prudently managing risk and have adequate resources to meet their obligations.

Updated May 26, 2025.

Prudential Regulatory Authority (PRA 110)

PRA 110 is referred to as a regulatory reporting requirement brought about by the Prudential Regulation Authority (PRA) in the UK for regulating financial institutions, such as banks, building societies, PRA-designated companies, and UK branches of European Economic Area (EEA) companies. This reporting requirement, established 2019, aims to render the regulator a more granular and profound view of short-term liquidity risks encountered by financial institutions.

Characteristics of PRA 110:

1. Short-term Liquidity

PRA110 particularly targets liquidity risks within a short-term timeline, usually less than 30 days, elaborating the extent of the Liquidity Coverage Ratio (LCR) by giving a more elaborated day-to-day analysis for the initial months.

2. Evaluation of Risks

The report/return helps the PRA assess several core perspectives of liquidity risk. Key components are:

- Balance Sheet Data as an Input

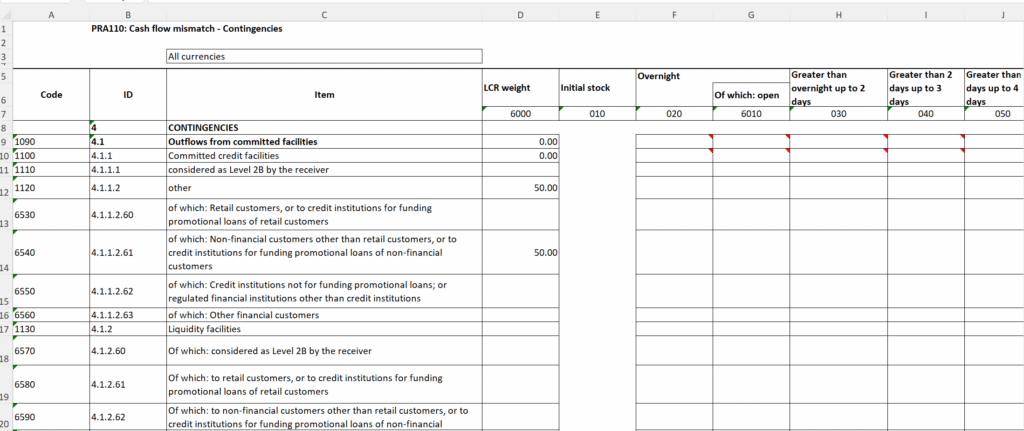

PRA 110 statutorily requires companies to report cash movements of contractual obligations and maturities (inflows and outflows) derived from both on-balance sheet entries (e.g., loans and deposits) and off-balance sheet exposures (e.g., contingent liabilities, unused credit lines, and guarantees).

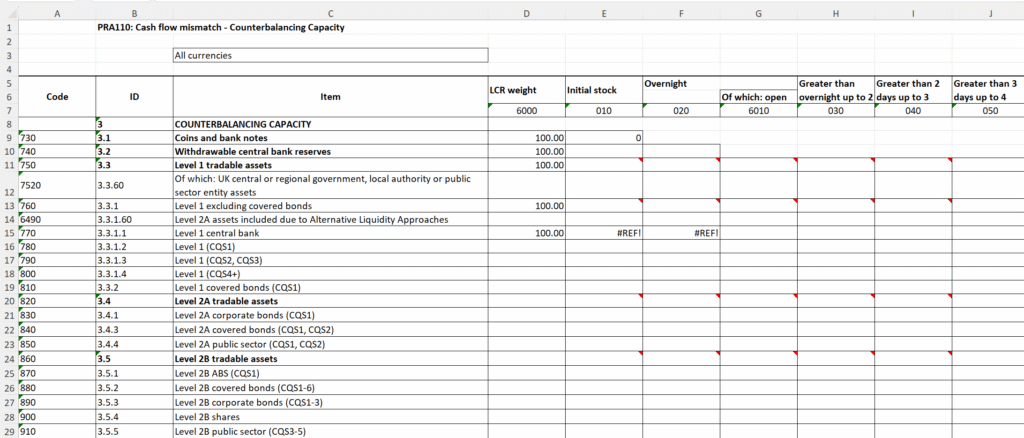

- Counterbalancing Capacity (CBC)

The aspect constitutes the stock of unencumbered or liability-free assets or other funding sources available for a company to cover potential contractual gaps, which are directly associated with assets contained on the balance sheet.

- Memorandum Entries

The aspect joins existing liquidity report requirements with new data points, encompassing details on derivatives and their connected associated margins, which are always related to off-balance sheet entries.

- Essence of Data Quality

The consistency and accuracy of data obtained from balance sheet and related off-balance sheet entries are germane for an error-free PRA 110 return/report.

- Data Requirements and Reporting Frequency

PRA 110 return is complex and requires essential data (including due diligence), typically with short processing and returning times. Larger companies (holding assets of around £25 billion (€30 billion) or above) must complete the return weekly, while smaller companies are required to do so monthly. In circumstances of heightened liquidity distress, the reporting frequency for some companies could be returned daily.

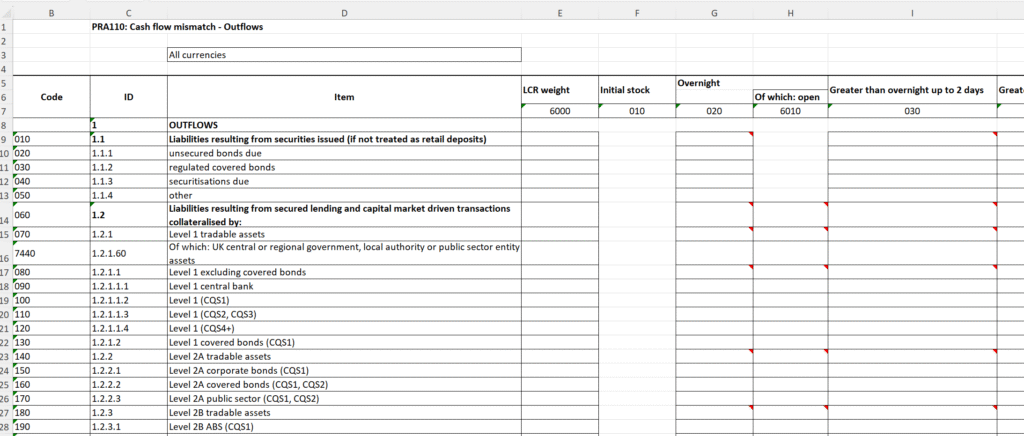

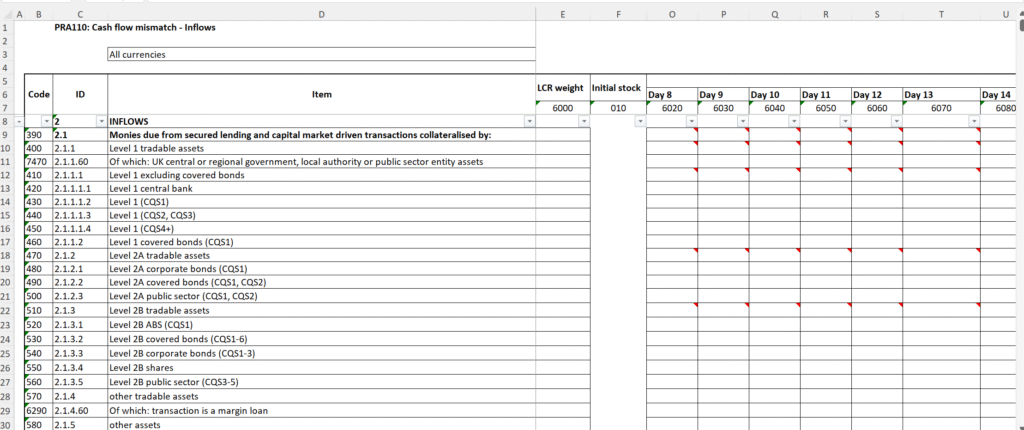

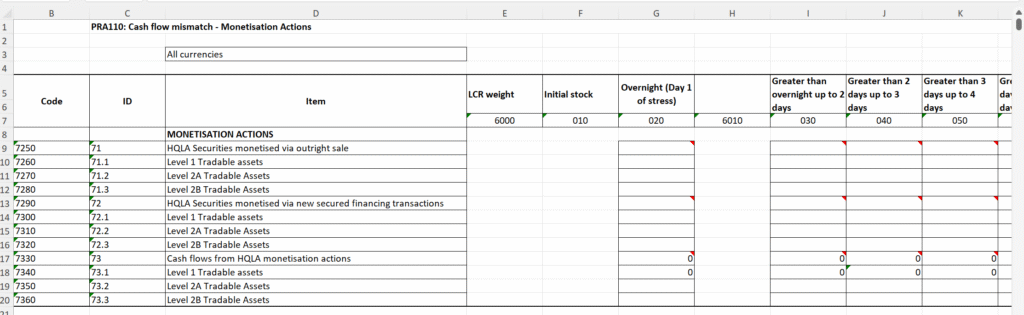

- Cash Flow Mismatch

In the perspective of PRA110, a cash flow mismatch represents the difference between a firm’s cash inflows and outflows over stipulated time horizons, specifically under stress scenarios. The PRA110 monitors short-term liquidity risks and potential stress within financial institutions, such as banks and building societies.

Specifically, a cash flow mismatch indicates whether a firm has adequate cash flow monetized liquid assets and other inflows to cover its outflows (daily basis), under stressed scenarios. The PRA110 return reveals situations where:

- A bank may hold inadequate High Quality Liquid Assets (HQLA) to meet topmost liquidity needs within a 30-day period.

- A bank may be unable to readily convert its non-cash HQLA into cash quickly enough to cover cumulative or culminating net outflows under a stress situation, based on the framework of Liquidity Coverage Ratio (LCR).

- Helps to identify potential weaknesses and vulnerabilities in liquidity risk management, including to monitor intraday risks and timing mismatches.

- Complexities and Challenges: Owing to the comprehensive nature and tight deadlines, executing and managing the PRA110 return can pose challenges for financial institutions. Efficient management of data, viable processes, and proficient resources are significant to ensure compliance.

PRA 110 Spreadsheets