Simple Interest Calculations

Present Value

Yield on a Investment or Cost of a Borrowing

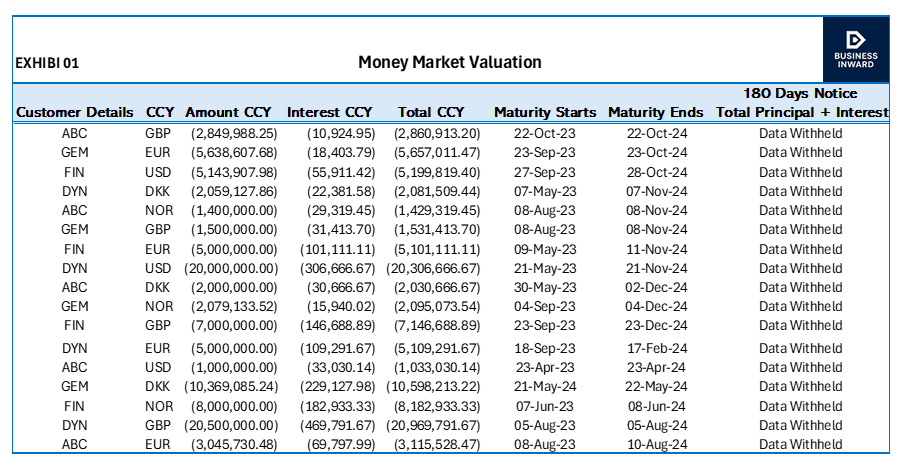

Money Market Loan Spreadsheet

Deposits & Coupon-Bearing Instruments