Liquidity Coverage Ratio (LCR)

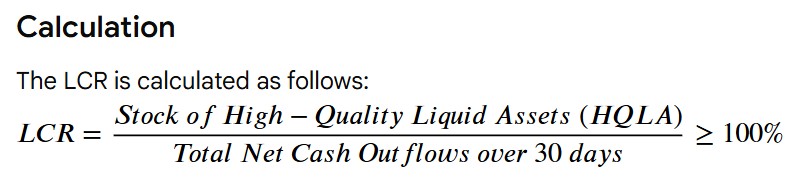

The LCR is a requirement from the Basel framework that mandates banks to hold a minimum level of high-quality liquid assets (HQLA) to cover their total net cash outflows over a 30-day, hypothetical stress scenario. It guarantees a bank can survive a substantial liquidity crisis by having adequate easily convertible cash to meet obligations during this short period, with the minimum requirement being 100%. The ratio is calculated by dividing the bank’s stock of HQLA by its total net cash outflows over a 30-day stress period.

Key components:

- High-Quality Liquid Assets (HQLA): Assets (cash and cash equivalents) that can be converted into cash easily and immediately with little or no loss in value.

- Total Net Cash Outflows: The difference between a bank’s total expected cash outflows and total expected cash inflows over the 30-day period, under a severe stress scenario.

Updated 02 November, 2025.

LCR Stress Scenarios

Components of LCR stress scenarios:

- Deposit outflows: A loss of both insured and uninsured deposits, as seen in the 2023 banking turmoil, is a key stress scenario. The LCR accounts for this by assuming a specific outflow rate for different types of deposits; for stable retail deposits, it might assume a 5% outflow rate during the 30-day stress period.

- Wholesale funding stress: A considerable reduction in a bank’s ability to raise funds in wholesale markets. This could involve a decline in secured financing availability or an inability to roll over short-term debt.

- Credit rating downgrade: A downgrade can result in a loss of market access and risen costs for borrowing. This can also trigger collateral calls on some derivatives or secured financing arrangements, further rising outflows.

- Drawdowns on credit and liquidity lines: A stress scenario assumes that a portion of off-balance sheet commitments, such as credit and liquidity lines to customers, will be drawn down. This is calculated by applying a specific drawdown rate to the total outstanding amount.

- Market-wide shocks: These are more profound events that affect multiple institutions, such as a general “flight to quality” where investors move out of riskier assets and into safer ones, such as U.S. Treasury bonds.

- Idiosyncratic shocks: These are events specific to one institution, such as the failure of a large counterparty or a rumor that causes a run on that specific bank’s deposits.

How these scenarios impact the LCR:

- Increased net cash outflows: The LCR is designed to measure a bank’s ability to withstand a crisis. The assumed outflow rates for deposits and other liabilities during a stress scenario are applied to their current balances to determine the total net cash outflows.

- Reduction in HQLA: While the stock of HQLA is meant to be a buffer, the stress scenario implies that the value of some assets may decline, and the ability to convert them to cash might be hindered.

- LCR drop below 100%: In a severe stress scenario, the estimated net cash outflows could exceed the stock of HQLA, causing the LCR to fall below the 100% minimum requirement. Banks are expected to report immediately if their LCR falls below 100%.