Insurance Industry Regulation

In insurance industry regulation refers to the laws, rules, and standards that govern how insurance firms operate to protect consumers and make ensure financial stability. In UK, insurance industry regulation is overseen by the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA). This encompasses regulating an insurer’s financial health (prudential regulation), how they treat customers and conduct business (conduct regulation), including the suitability of the individuals managing insurance companies. The framework is fundamentally based on the Financially Services and Markets Act 2000, with with specific rules set established by the PRA and FCA, such as the Solvency II regime for financial requirements and the Senior Managers and Certification Regime (SM&CR) for individuals.

Updated 24 October, 2025.

Aspects of Insurance Regulation

- Dual regulators: The PRA supervision is centered on the safety and soundness of insurers, while the FCA focuses on how they conduct business and the integrity of the market.

- Financial stability: Regulations, such as Solvency II mandate that insurers have adequate capital and vigorous risk management systems to ensure they can meet their obligations.

- Consumer protection: Rules are in place to ensure customers are treated fairly, which includes lucid policy terms, sincere advertising, and equitable claims handling.

- Individual accountability: The Senior Managers and Certification Regime (SM&CR) holds senior individuals within companies personally accountable for their responsibilities.

- Authorization and oversight: To operate, insurers must be authorized by the PRA and meet specific threshold conditions. Regulators have powers to intervene, investigate, and sanction companies and individuals.

- Legal basis: The core legislation is the Financial Services and Markets Act 2000, which describes the powers and requirements for authorized firms.

Risk-Based Capital and Requirements

Risk-based capital (RBC) constitutes the amount of capital a financial institution must hold to cover potential losses dependent on the specific risks it undertakes. This requirement is ascertained by evaluating a company’s unique risk profile, as well as asset, credit, and underwriting risks, to ensure it has adequate capital to protect policyholders or depositors from insolvency. The objective is to align the required capital more closely with the actual risk, rather than using a one-size-fits-all mechanism.

RBC requirements are financial protections for insurance companies and banks to ensure they can withstand unexpected losses.

- Risk-based Capital Ratio (RBC) = (Available Capital / RBC Requirement)×100

The RBC Requirement is the sum of capital charges for various risks, calculated by multiplying exposures (such as assets or reserves) by regulatory factors for each risk category, which can include underwriting, credit, asset, and business risks.

Solvency II European-Based Regulation

Solvency II is the harmonized, risk-based prudential regulatory framework for insurance and reinsurance undertakings in the European Union (EU), and onshored and brought into the UK market. It began fully applicable on January 1, 2016, and replaced former directives (Solvency I) to establish a single market for insurance services in Europe.

Characteristics and Objectives Solvency II

- Risk-Based Approach: Capital requirements are associated with directly to the risk profile of each individual firm, fostering better risk management.

- Market-Consistent Valuation: Assets and liabilities (especially technical provisions for future claims) must be valued at the amount for which they could be exchanged or settled on the market, providing a realistic balance sheet assessment.

- Proportionality: The rules are designed to be applied in a manner proportional to the nature, scale, and complexity of the risks within an insurer’s business, with less strict rules for smaller, less complex companies.

- Improved Governance and Risk Management: The framework mandates strict requirements for internal controls, risk assessment (through the Own Risk and Solvency Assessment – ORSA), and the apt and proper criteria for core personnel.

- Transparency and Disclosure: Insurers are required to report detailed data to supervisory authorities and disclose key aspects of their financial health and risk management to the public, promoting market discipline.

The Three Pillars

- Pillar 1: Quantitative Requirements:

- This pillar established rules for valuing assets and liabilities, computing technical provisions, and ascertaining capital requirements.

- It describes two capital levels: the Minimum Capital Requirement (MCR) and the more risk-sensitive Solvency Capital Requirement (SCR), calibrated to ensure an insurer can meet its obligations with a 99.5% confidence level over one year. MCR absolute floor of €2.7 for non-insurance undertakings and €5 for insurance are required.

- Pillar 2: Governance and Supervisory Review:

- This pillar sets out qualitative requirements for an insurer’s systems of governance and risk management.

- It includes the requirement for companies to conduct their own forward-looking Own Risk and Solvency Assessment (ORSA) and provides national supervisors with powers to challenge and intervene in a company’s risk management practices.

- Pillar 3: Reporting and Disclosure:

- This pillar focuses on transparency through supervisory reporting (Regular Supervisory Reports – RSR) and public disclosure (Solvency and Financial Condition Reports – SFCR).

Valuation of Assets and Liabilities

In the UK, the relevant requirements for the valuation of assets and liabilities for majority of insurance companies are fundamentally the responsibility of the Prudential Regulation Authority (PRA), not the Financial Conduct Authority (FCA). The FCA focuses on business business conduct and consumer protection, as well as ensuring products give fair value to customers.

The core regulatory framework for the valuation of assets and liabilities is adopted from the Solvency UK regime (formerly Solvency II in the EU).

Valuation of Assets

- General Principle: Assets must be valued at the amount for which they could be exchanged between knowledgeable, willing parties in an arm’s length transaction (i.e., fair value).

- Valuation Hierarchy: A hierarchy of valuation methods must be followed:

- Level 1: Quoted market prices in active markets for the same assets are the primary and most reliable method.

- Level 2: If Level 1 data is unavailable, quoted market prices for similar assets, with adjustments for differences, are used.

- Level 3: Where active market data is scarce (common for illiquid or alternative assets), valuation techniques using observable market inputs to the greatest extent possible are applied.

- Level 4: Only if no observable inputs are available can company-specific, unobservable inputs be used, provided they reflect market participant assumptions.

- Prohibited Methods: Valuation at historical cost or amortized cost is generally prohibited for solvency purposes.

Valuation of Liabilities

- General Principle: Liabilities are valued at the amount for which they could be transferred or settled between knowledgeable, willing parties in an arm’s length transaction.

- Technical Provisions: The primary liability for insurers is technical provisions (future claims and policyholder benefits), which are calculated as the sum of a best estimate of future cash flows (discounted using a relevant risk-free interest rate) and a risk margin.

- Solvency: Firms must maintain adequate financial resources (capital and liquidity) to meet all their liabilities as they fall due, which requires realistic valuation bases for assets and liabilities.

- Contingent and Prospective Liabilities: The valuation of liabilities must include contingent and prospective liabilities and claims that should be paid in the interest of fair treatment of customers, even if not legally enforceable. Material contingent liabilities must be recognized and valued based on the discounted present value of future cash flows, a stricter approach than some accounting standards.

- Matching Adjustment (MA): For long-term life insurance business, the PRA permits a “matching adjustment” to the discount rate used for liabilities, allowing firms to recognize the illiquidity premium from holding long-term, illiquid assets that match those liabilities.

Best Estimate (BE) and Risk Margin (RM)

Under the Solvency II regulatory framework, which governs insurance companies in the EU (and serves as a model elsewhere), the technical provisions are the sum of the best estimate (BE) and the risk margin (RM). The formulas for these components are based on projected future cash flows and capital requirements.

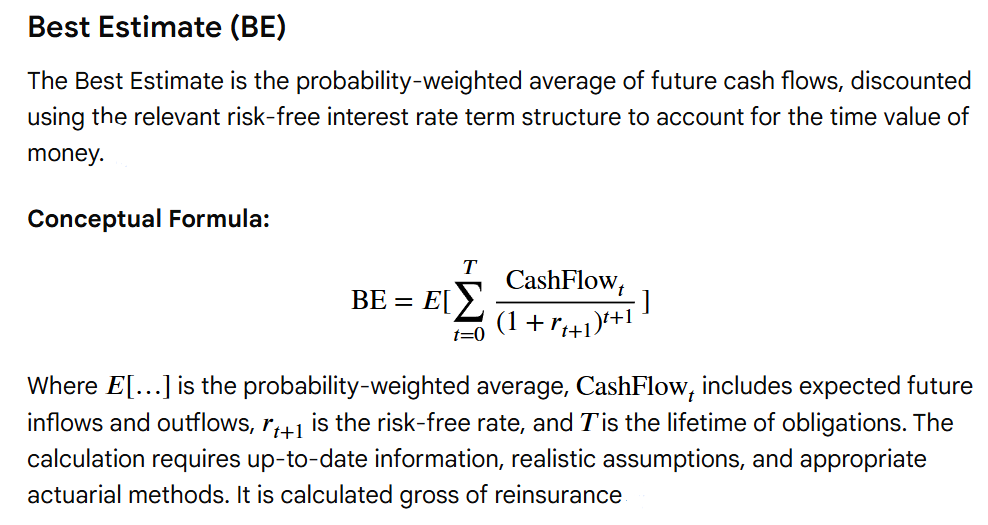

Best Estimate (BE)

Risk Margin (RM)

Own Funds of Insurance Companies

Own funds are an insurance firm’s regulatory capital, comprising basic (on-balance sheet) and ancillary (off-balance) and items, which is used to meet its capital requirements, fundamentally the Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR). These funds must be adequate to absorb unexpected losses and make sure claims can be paid, even in adverse circumstances. They are tiered based on quality, with Tier 1 being the highest.

Components of Own Funds

- Basic Own Funds: Capital available directly on the balance sheet.

- Tier 1 Capital: Highest quality, most permanent, and loss-absorbing capital.

- Tier 2 Capital: Subordinated capital with a fixed, long maturity date.

- Tier 3 Capital: Lowest quality capital, with a shorter maturity of 5 years or less.

- Ancillary Own Funds: Items that require supervisory approval before they can be used to absorb losses.

- Unpaid share capital or initial fund

- Letters of credit and guarantees

- Legally binding commitments

- Absorb losses: The primary purpose of own funds is to absorb unexpected losses to protect policyholders.

- Meet capital requirements: Insurers must possess own funds at least equal to their Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR).

- Ensure solvency: If an insurer’s own funds are adequate to meet its required solvency margin, it may encounter supervisory consequences.

- Tiering: Items are tiered based on their quality, permanence, and ability to absorb losses.

- Availability: Rules limit the amount of each tier that can be held to ensure funds are available when needed.

- Regulatory approval: Ancillary own funds must have prior supervisory approval to be recognized as part of the insurer’s capital.

SCR and MCR

- Purpose: A risk-sensitive measure designed to absorb unexpected losses over a one-year period with a 99.5% confidence level. It acts as a buffer against extreme but plausible events.

- Calculation: Can be computed using the regulator’s standard formula or an insurer’s approved internal model.

- Intervention: Falling below the SCR triggers a tiered intervention process from the regulator.

- Purpose: The absolute minimum level of capital an insurer must hold. Falling below this level triggers immediate regulatory intervention.

- Calculation: Calculated using a linear formula based on factors like technical provisions and written premiums, with an 85% confidence level over one year.

- Relationship to SCR: It is capped at 45% and has a floor of 25% of the SCR. Additionally, there is an absolute minimum floor that varies by insurer type.

- Reporting: Insurers must calculate and report the MCR to the PRA at least quarterly.

Differences and Relationship