Earnings forecasts are dependent on analyst’s targets or forecasts company profitability and growth of projects and investments that a company plans to take on during the upcoming year. This process commences with forecasts of the project’s future end results for the company. Some of the end results will impact the company’s revenues; others will impact its costs.

Updated 24 June, 2025.

Revenue and Cost Estimates

In capital budgeting, revenue and cost estimates aim at forecasting the long-term cash flows related with major investment, encompassing initial project costs, current operational expenses, and future revenue streams. These estimates are applied in valuation methods, such as Net Present Value (NPV) and the Internal Rate of Return (IRR) to ascertain if the projected returns rationalize the investment and exceed a pre-established or fixed hurdle rate, which represents the minimum allowable rate of return on a project.

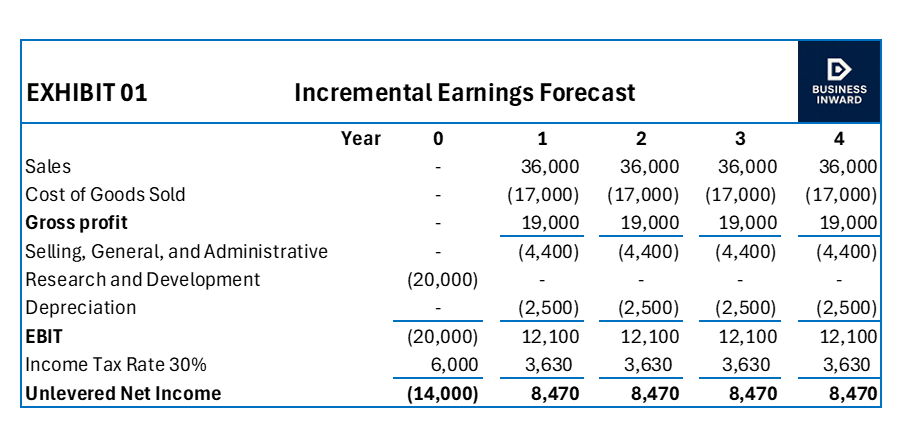

Incremental Earnings Forecast

Incremental earnings forecast of a capital budget predicts a project’s additional net income by finding out project-specific revenues and costs, excluding sunk costs. Precisely, incremental earnings are expected change arising from undertaking a new project. This forecast is significant for capital budgeting to ascertain if a project’s incremental earnings will give rise to returns to rationalize the investment.

Capital Expenditures and Depreciation

Forecasting capital expenditures (CapEx) and depreciation is essential for computing a project’s incremental earnings, with CapEX being the cash constitutes the cash expended on assets and depreciation the non-cash cost that spreads over life of asset.

Indirect Effects on Incremental Earnings

When calculating the incremental earnings of an investment decision, all changes between the company’s earnings with the project versus without the projects.

Opportunity Costs: The opportunity cost of utilizing a resource is the value it could have generated in its best alternative use. Given that this value is lost when the resource is utilized by another project; thus, the opportunity cost should be included as an incremental cost of the project.

Project Externalities and Cannibalization

Project externalities are indirect impacts of the project that may rise or fall the profits of other business activities of the company. Cannibalization occurs when sales of a new product dislodge sales an existing product. When developing a new product, companies are often concerned about the cannibalization of their existing products. However, if sales are likely to fall in any case due to new products introduced by competitors, then these lost sales are a sunk cost and should not be included in projections.

Sunk Costs and Incremental Earnings

A sunk cost is referred to as any unrecoverable cost for which a company is already liable. Sunk costs have been or will be paid regardless of the decision as to whether or not to proceed with the project. Thus, sunk costs are not incremental in relation to the current decision and should not be included in incremental analysis.