The Credit Underwriting Process

The credit underwriting process is a lender’s detailed assessment of a borrower’s financial ability to repay a loan, entailing evaluating credit history, income, debt-to-income ratio, and collateral. This process commences with an application and submission of documents, ensued by data analysis using manual review or automated systems to identify risks.

Borrower’s information is verified by the underwriters, and established creditworthiness based on established standards, and then make final decision to approve, reject, or request additional information prior to the finalization of the loan.

Updated 22 August, 2025.

Credit Initiation

Either a lender or borrower approaches for a loan or a relationship manager (or accountant) searches for a prospective loan customer in line with is sales effort. The credit initiation process makes sure that the loans facilitated by a lending institution conform with the lender’s enterprise-wide credit policy, guidelines, credit procedures, including credit standards.

Credit Analysis

A vital objective of the process is to assess the credit risk, which has two components: the borrower’s ability to repay the loan and the collateral upon which the loan is based. The conventional “Five Cs” method is a good starting point for a deeper dive into credit risk rating methodology.

The Five Cs:

1. Capacity

The ability to repay a loan is the borrower’s financial capacity to repay a loan with interest as at when due. To assess capacity, reliable and timely financial statements are needed.

2. Capital

Capital means shareholders’ equity in the enterprise. It represents what the owners of the company have invested and what they have at risk should the business fails. Thus, the credit analysis includes the regulatory capital and economic capital:

- Regulatory capital is the capital that banking authorities interpret for regulatory purposes, and items in the interpretations or definitions are balance sheet items.

- The economic capital of a bank is derived from an economic capital model that does not need assets as inputs. It constitutes the difference between percentile of a loss distribution and the expected loss derived from combining the probability of default (PD) and the loss given default (LDG).

The primary source of repayment is cash flow. The secondary source of repayment is collateral in case the borrower defaults to repay the loan through cash flow. Personal assets, paper assets, physical assets, and even future income (e.g., customers’ orders) are all deemed collateral. A borrower would pledge the assets to secure a loan. In the event of default, the principal concern of the lender of a secured loan is whether the realizable value of the collateral is adequate to cover the expected loss.

4. Condition

The willingness to grant a loan is dependent on some conditions that are external to the lender. The relationship manager and the credit analyst must be conversant with recent and emerging trends in the borrower’s line of work, the borrower’s industry, business conditions influencing sales, and economic drivers, such as interest rates and inflation that could affect the loan.

5. Character

An evaluation of an obligor’s credit history is critical to determine desire to repay a loan. A poor credit history is a good predictor of future repayment difficulties. Thus, reputation for repaying debt is an important part of character evaluation.

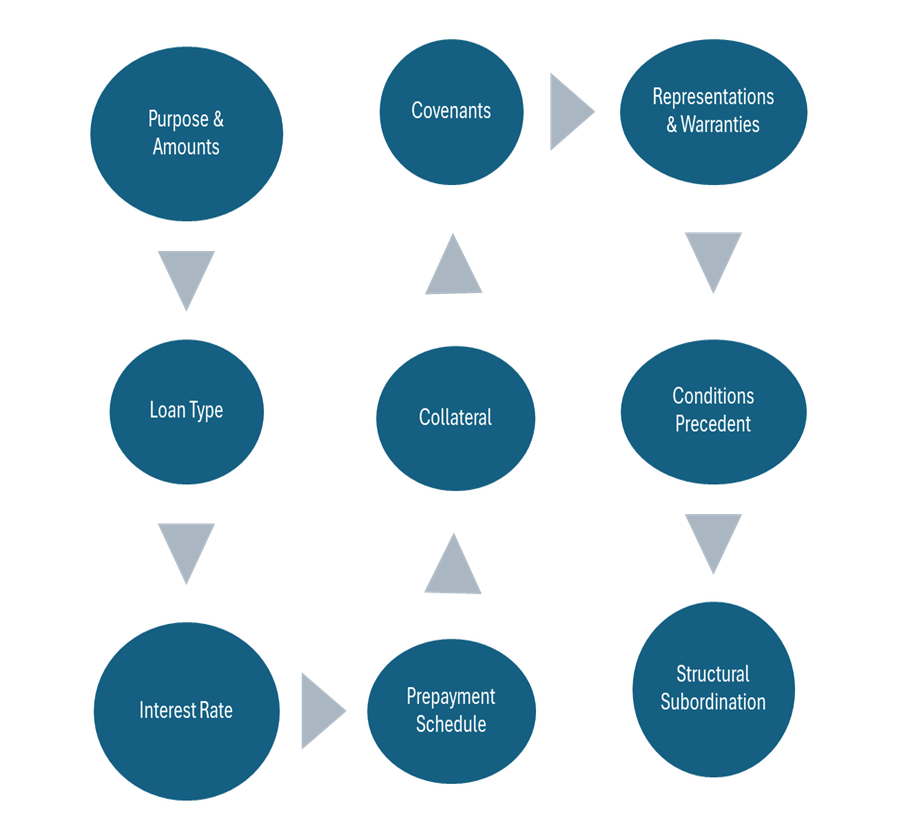

Loan Structuring

Loan structuring is the process of defining and negotiating the specific terms and features of a loan agreement to meet the requirements of both the borrower and the lender, paying attention on factors, such as interest rates, repayment schedules, collateral covenants, and the entire loan amount.

Loan structuring is an customized approach aimed at aligning the loan’s characteristics with the borrower’s financial situation and the lender’s risk appetite, making ensure that the structure is suitable for the loan’s objective and lessens potential risks for both parties.

Key Elements of Loan Structuring

Credit Submission

The business unit prepares and submits a transaction request (TR) to Risk Management for adjudication. This document outlines the “deal”. A typical TR would likely include:

- Transaction Details: This section includes customer information, such as renewing date of the Risk Assessment (the BRR), renewing date of the Transaction Request that documents that total exposure under the name of the borrower, the facilities requested (facility risk ratings, facility terms, the pricing, and different codes for portfolio monitoring. The structuring: the amount of loan requested, when the funds will be disbursed, and for how long the funds will be outstanding. Structuring encompasses whether the funds are committed facility (there is obligation for the lender to provide loan if the borrower meets requirements) or uncommitted facility (no obligation to provide loan).

- Transaction Outline: This section defines the rationale for the loan, exceptions to credit policy and request for waivers, the strengths and weaknesses of the transaction, and the means through which the lender will reduce the identified risk.

- Transaction Monitoring and Reporting: This section provides instructions on how the account will be scrutinized in order to discover and reduce risk, and protect the interests of the lender. The instruction would encompass: (i) Early Warning Signals, (ii) Financial Covenants and the computation method, (iii) reporting covenants for financial statements, certificates, environmental reports, (iv) The frequency and timing of reports, the accountabilities, and responsible parties, such as the business unit (front office) and the loss servicing unit (back office), (v) Pre-disbursement conditions, and (vi) Margin calculations.

Loan Documentation

Thorough documentation is a crucial component of the underwriting process given that loan documents serve as the lender’s fundamental protection once it pays out the loan. If documents are not in perfect order, there is potential for loan losses. The legal departments of a bank, or outside counsel, prepares the important documentation for signing by all parties to the agreement.

Loan Closing & Credit Disbursement

The closing means the date and time that a loan becomes final and the lender pay out a loan. At the closing, both the lender and the borrower sign various legal documents binding both parties to the loan agreement. The closing of the loan signifies that the borrower is legally required to repay the loan an the lender is legally committed to advance funds (or tranches of funds) subject to the loan conditions.

Prior to the lender disbursing funds into the borrower’s account, the lending service unit of the financial institution must ensure that pre-disbursement requirements in the approved TR are fulfilled.

Loan Monitoring & Reporting

The monitoring process commences once the lender disburses the loan and the monitoring requirements that encompass the kinds of reports and the frequency of the reporting are outlined in the Loan Agreement. Banks have monitoring systems in place and the borrower is required to submit financial and other information on a regular basis.

Problem Loan Management

As a rule, a problem loan is one that cannot be repaid according to the original terms of the loan agreement. in the Basel Committee on Banking Supervision (BCBS) framework, problem loans come under the rubric of non-performing loans. BCBS describes these loans that “the bank deems the obligor is unlikely to repay its credit obligations to the banking group in full, without recourse by the bank to actions such as realizing security (if held).