Consolidated Financial Statements

Consolidated financial statements offer a unified view of a company’s financial position across subsidiaries and investments. This section breaks down the complexities of combining entities, managing foreign operations, and handling goodwill and non-controlling interests. Whether you’re navigating mergers or preparing comprehensive reports, these insights equip you to interpret and present financial information with accuracy and confidence in a dynamic business environment.

Updated 30 June, 2025.

Business Acquisitions and Combinations

Method 1: Acquisition of Net Assets

The acquisition of net assets, in the context of business combinations or mergers and acquisitions (M&A), is referred to as the process of a company acquiring the net assets (assets minus liabilities) of the acquired company. The net assets are normally valued at fair value, and the difference between the purchase price and the fair value of the net assets can result in goodwill or a bargain purchase.

Method 2: Acquisition of Shares

A share acquisition (a share purchase or share sale), is a transaction where one entity (the buyer) purchases shares in another company (the target) to gain ownership or control that typically determined by the percentage of ownership.

Business Combination, IFRS 3

IFRS 3, “Business Combinations,” mandates the accounting treatment for acquisitions of businesses. It outlines how an acquirer recognizes and measures assets, liabilities, and goodwill in a business combination, using the acquisition methods. Fundamentally, it provides a framework for accounting for takeovers, mergers, and other transactions where one entity gains control of another.

IFRS 3 establishes principles and requirements for how an acquirer in a business combination:

- recognises and measures in its financial statements the assets and liabilities acquired, and any interest in the acquiree held by other parties;

- recognises and measures the goodwill acquired in the business combination or a gain from a bargain purchase; and

- determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects of the business combination.

Purchase Consideration

Purchase consideration refers to the aggregate value of everything an acquiring company gives to a selling company in exchange for the assets or business being acquired. It is importantly the price the buyer pays to take ownership of seller’s assets or business. This consideration can be cash, shares of the acquiring company, deferred consideration (valued at present value of the future payment), or a combination of these.

Example:

Jack Plc acquired 90% of the ordinary shares of Sharon Ltd on 1 October 2010 for the following considerations:

- the issue of two million £1 ordinary shares at market value £1.80;

- an immediate cash payment of £200,000; and

- a cash payment of £500,000, three years after the date of the acquisition.

Jack Plc can borrow funds at 10%.

Journal entry to record the purchase consideration in the financial statements of Jack plc:

Accounting for Investments

The accounting for investments involves tracking, measuring, and reporting and compliance (GAAP & IFRS) on the value of investments to understand profit and loss, tax reporting, risk and the overall effect on an organisation’s financial performance. Investment measurements can be done through equity method (e.g., 20%-50% ownership), fair value method (for trading or available for sale), and cost method (non-controlling stakes, less than 20% ownership).

Subsidiary

IFRS 10 Consolidated Financial Statements defines a subsidiary as an entity that is controlled by another entity (the parent company).

Example 1:

Johson Co acquires more than 50% of the voting rights of another entity (Judin Co) and decision-making is resolved by voting rights.

On 1 September 2005, Johnson Co acquired £2.4m of the ordinary shares of Judin Co. At that date Judin Co had £3m ordinary shares in issue. Thus, Johnson Co has acquired an 80% holding (£2.4M/£3m = 80%).

Associate

IAS 28 Investments in Associates and Joint Ventures defines an associate as an entity over which the investor has significant influence. The significant influence is the “power to participate in the financial and operating policy decisions of the investee but is not control of those policies.

On 1 January 2005, Akin Ltd acquired 80m of the 200m ordinary shares in issue by Orange Ltd. Akin Ltd has now acquired an associate, because it has acquired between 20% and 50% of the voting right shares.

Joint Venture

IAS 28 Investment in Associate and Joint Ventures defines a joint venture as a “joint agreement whereby the parties that have joint control of the agreement have rights to the net assets of the agreement.

On 1 February 2005, Soso Ltd and Asun Ltd, entities that are related, acquire 50% each of the ordinary shares of Gogo Ltd and will jointly control the agreement.

Trade or Simple Investment

A trade or investment occurs where an investor acquires less than 20% of the voting rights of the investee and the investment can be considered to bring about a significant influence.

Accounting Standards for trade investment are the IFRS 9 ‘Financial Instruments’ and the IAS 39 ‘Financial Instruments Recognition and Measurement’. The standard encompasses requisites for recognition and measurement, impairment, derecognition, and general hedging accounting.

The Consolidated Statement of Financial Position: Complications

In business, group entities trade between themselves and subsidiaries pay dividends to parents. Often, some group entities owe amounts of money payable to other entities at a reporting date. Such situations give rise to a set of adjustments that are termed ‘complications’.

The Complications

- Unrealised inventory profits.

- Unrealised profit on sale of tangible non-current assets.

- Revaluation of a subsidiary’s net assets at acquisition.

- Proposed preference dividends by a subsidiary.

- Proposed ordinary dividends.

- Intragroup balances.

- Impairment of goodwill.

- Preference shares in issue by a subsidiary.

Complication 1: Unrealised Inventory Profits

IAS 2 Inventories states that inventories should be measured at the lower of cost and net realisable value. When a group entity sells goods to another at a profit and part or all the goods are in the inventory of the buying entity at the reporting date, and section of unrealised profit is added to the closing inventory of the group.

Example

James Ltd owns 75% of the share capital of Shawn Ltd. James buys goods for £10,000 and sells them to Shawn Ltd for £15,000. At the reporting date, Shawn Ltd still has the goods in inventory. In Shawn Ltd’s statements of financial position (SoFP), the goods are valued at cost of £15,000 in with IAS 2. If the inventory of Shawn Ltd were consolidated (without adjustment) with the inventory of James Ltd, the outcome would be that the group purchased the goods for £10,000 and valued its inventory at £15,000 which contravenes IAS 2. There is unrealised profit from a group perspective of £5,000.

The journal accounting treatment, by eliminating the unrealised profit:

Goodwill and Non-controlling Interests

Gosh Ltd acquired 65% of the ordinary shares of Maron Ltd on 1 October 2021 when the issued share capital of Maron Ltd was £3 million and its retained earnings £1 million. The consideration is as follows:

- the issue of one million ordinary £1 shares in Gosh Ltd at market value £2.25;

- a cash payment of £450,000 on 1 October 2023.

Gosh Ltd can borrow funds at 12%.

The non-controlling interests in the net assets of Maron Ltd as at 1 October 2021 is valued at £1,750,000.

Solutions:

Journal entry to record purchase consideration:

Foreign Operations

Translation of a Foreign Operation

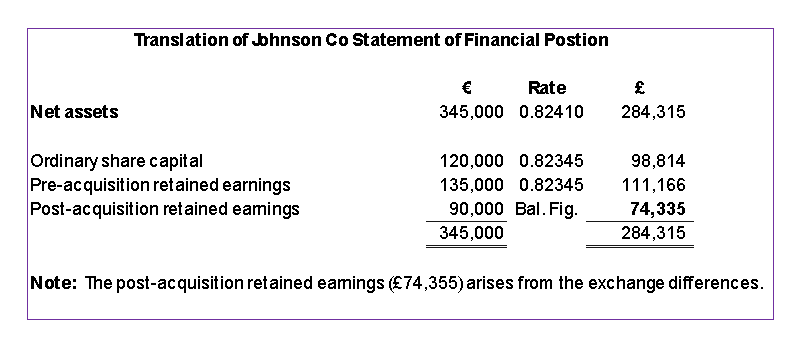

Under IAS 21, a reporting entity must translate the financial statements of a foreign operation into its own functional currency (reporting currency) prior to preparing the consolidated financial statements. The translation rules of functional currency must comply with IAS 21, paragraph 39:

- Assets and liabilities should be translated at the closing date.

- Income and expenses should be translated at the exchange rate at the dates of the transactions, or at an average rate for the period with reasonable approximation.

- All resulting exchange differences should be recognised in other comprehensive income.

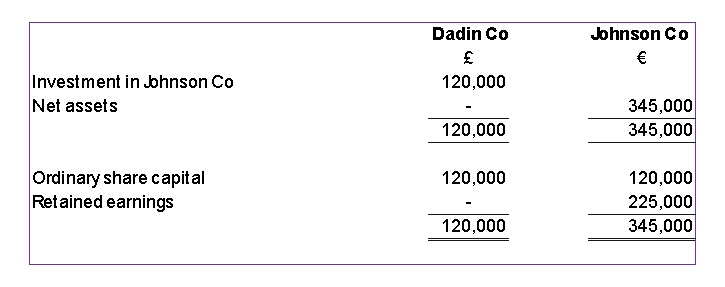

Example

- Dadin Co acquired 75% of the ordinary shares of Johnson Co on 01 September 2022 when the retained earnings of Johnson Co were €135,000.

- Non-controlling interests are measured at acquisition date at their share of the net assets of Johnson.

Relevant rates of exchange rate are:

- The functional currency of Dadin Co is the Pound Sterling while that of Jonhson is the Euro.

- Requirement: prepare the consolidated statement of financial position of Dadin Co. as at 31 August 2023.

Solution:

Consolidated a Subsidiary with Non-Controlling Interests

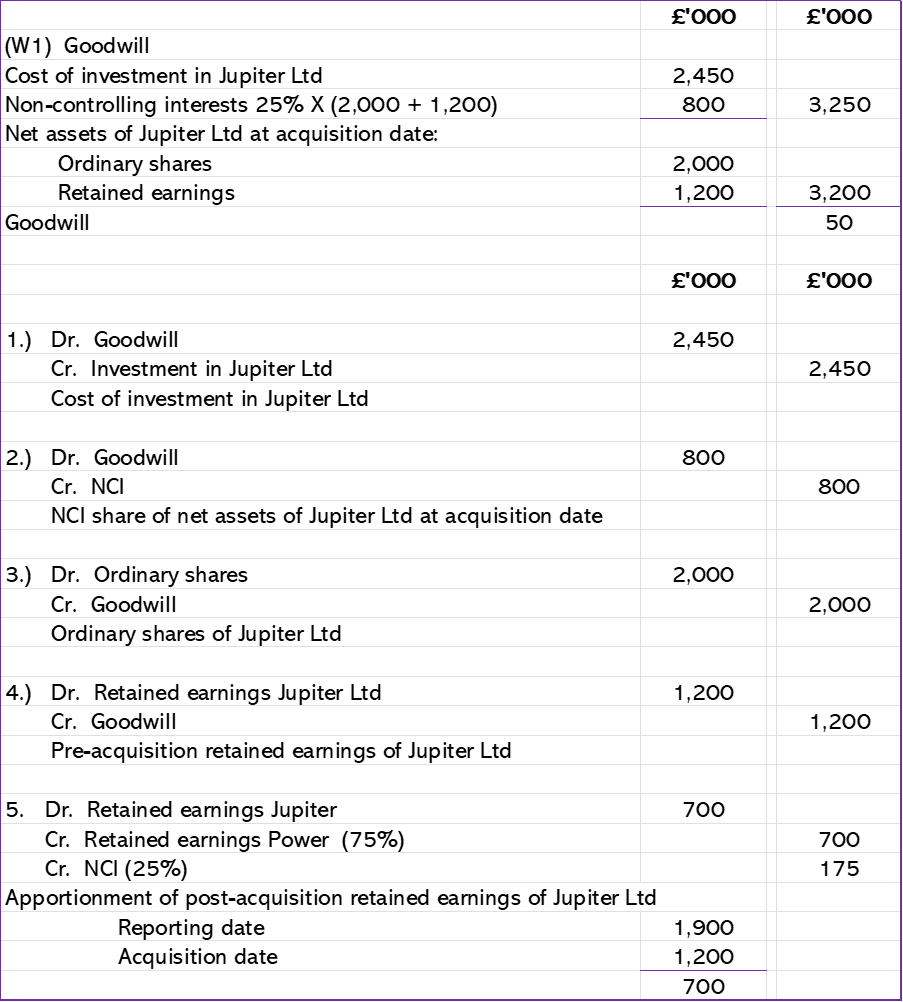

Example 6

Consolidating a subsidiary with non-controlling interests in preparation of a consolidated SoFP where Power Ltd owns less than 100% of voting shares of Jupiter Ltd.

Power Ltd acquired 1,500,000 shares in Jupiter Ltd in November 2021 when the retained earnings of Jupiter Ltd were £1,200,000.

Power Ltd chooses to measure non-controlling interests at their proportionate interest in the assets of Jupiter Ltd at the date of acquisitions.

Solution:

Group 1,500,000 / 2,000,000 = 75%

Non-controlling Interest (NCI) = 25%

Journal

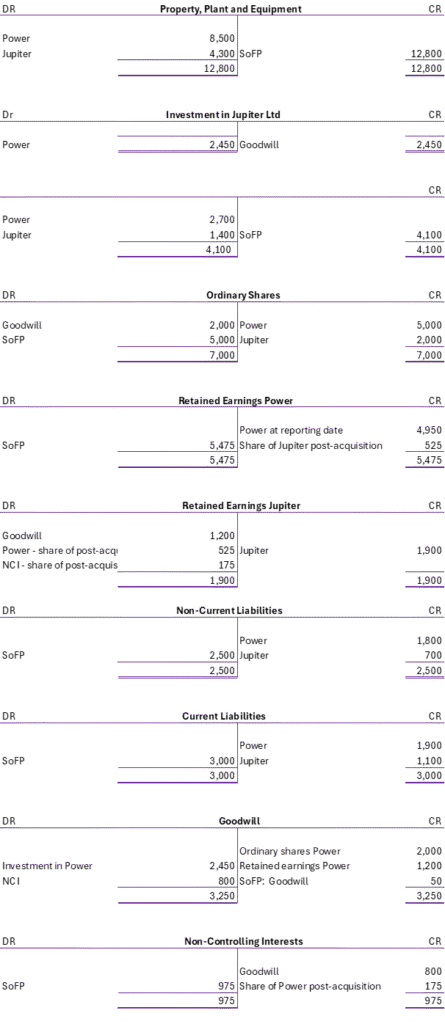

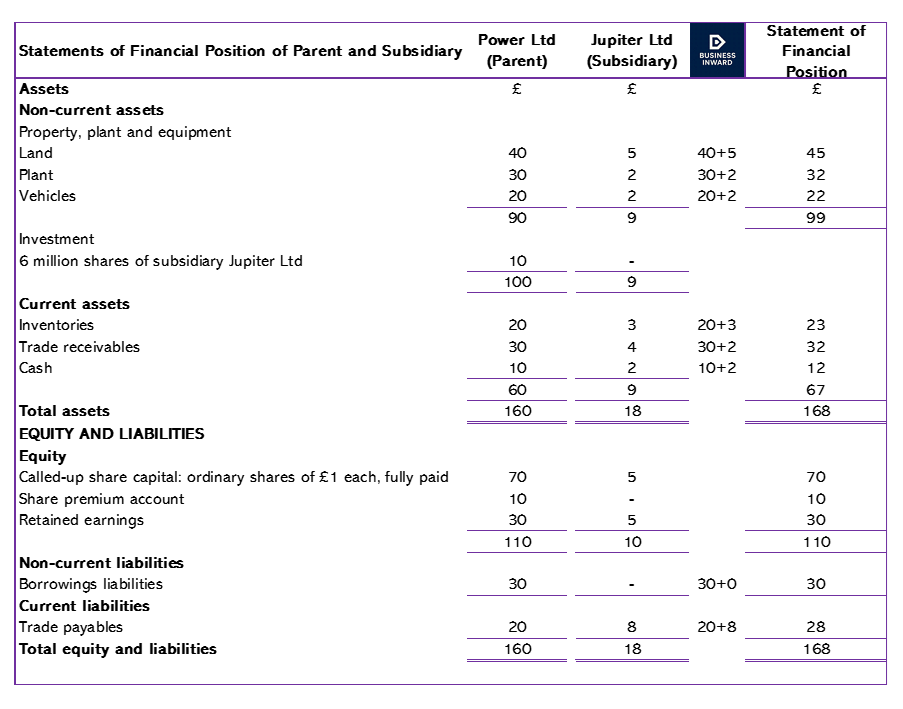

Preparing a Group Statement of Financial Position

The statements of financial position of Power Ltd (Parent) and Jupiter (Subsidiary), on the the former acquired all the shares in the latter, were as follows:

The equity section is group statement of financial position is solely that of Power Ltd (Parent). The 10 million equity for Jupiter Ltd (Subsidiary) cancels out with the 10 million that relates to 5 million shares of Jupiter Ltd (Subsidiary) in the non-current assets section of Power Ltd’s (Parent) statement of financial position. Given that power Ltd (Parent) owns all of the subsidiary’s shares.