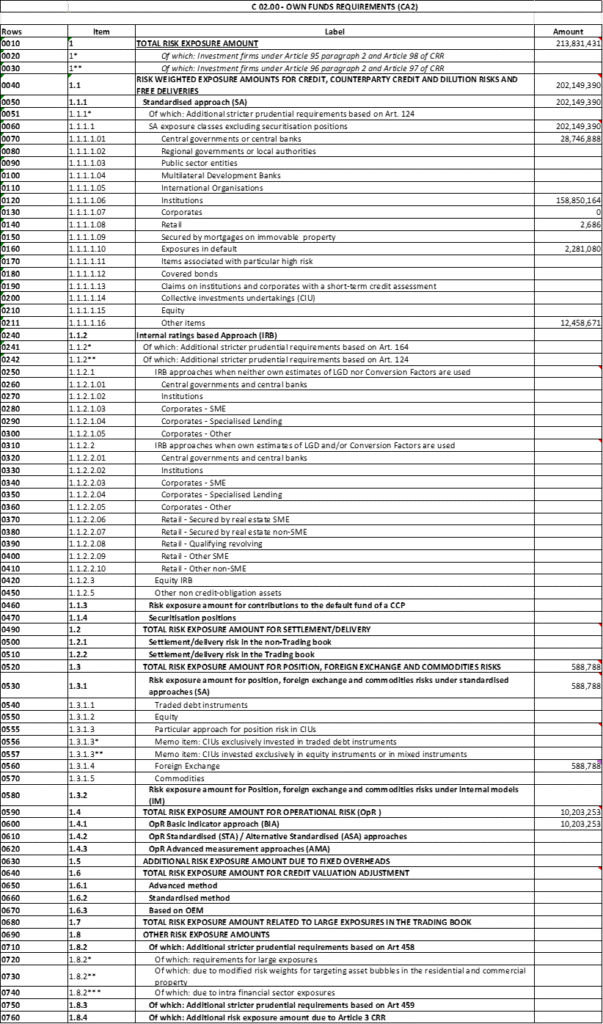

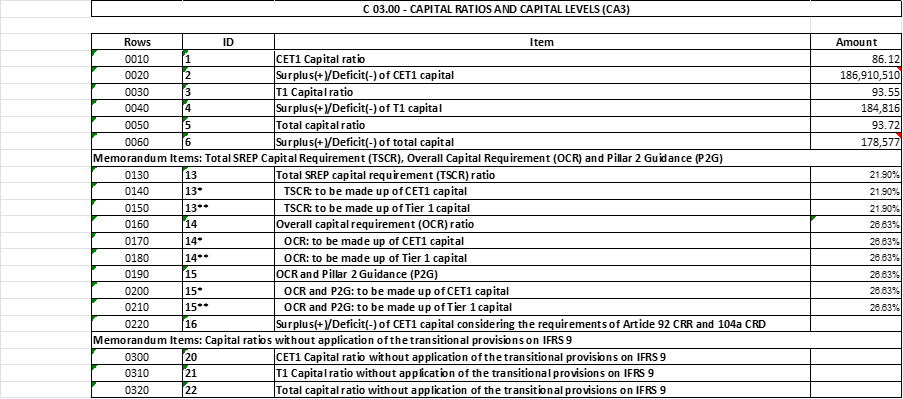

COREP (Common Reporting) is a standardized European regulatory framework for banks and investment entities to report capital adequacy (ordinary share capital and retained earnings), credit risk data, and other prudential information (capital returns, liquidity reports) to their national supervisory authorities. Requirements encompass reporting on capital, credit market, and operational risk standardized templates and XBRL, with monthly and quarterly submissions.

Updated 08 May, 2025.

Components of COREP CET1

1. Common Equity Tier 1 (CETI) Capital

CET1 represents the highest quality of a bank’s capital adequacy. In 2024 Q4, the UK capital adequacy ratio is 15.9%, as against 4.5% minimum capital adequacy ratio. This is a measure of core capital relative to risk-weighted assets, providing a safety net against financial losses.

CET1 capital encompasses the following core elements:

Common Shares:Paid-up capital from ordinary shares issued by the bank.

Stock Surplus:Share premium accounts resulting from the issue of common equity.

Retained Earnings:Profits the bank has accumulated and not distributed to shareholders.

Other Comprehensive Income (OCI): Some gains and losses not recognized in the income statement.

Other Reserves:Other reserves, encompassing those for general banking risks.

2. Purpose and Significance of CET1

Loss Absorption:

CET1 is established to be available immediately and without constraint to cover losses as they arise.

Bank Stability:

It functions as a critical safety cushion, supporting the bank to remain solvent and prevent failure during unstable economic cycle.

Protects Depositors:

By absorbing losses, CET1 safeguards depositors and other creditors.

Regulatory Requirement:

Regulatory authorities, such as those following the Basel III standards, oblige that banks sustain a minimum level of CETI capital as part of capital adequacy requirements.