Capital Structure/Liquidity Measures

Current Ratio

Current ratio is a financial metric used to evaluate a company’s ability to meet its short-term financial obligations. It is used to compare a company’s current assets to its liabilities. As a rule, higher current ratio indicates a better ability to pay off debts, while a lower ratio suggests potential liquidity difficulty.

- Formula for calculating current ratio: Current Assets / Current Liabilities

Interpretation:

- Ratio > 1: Suggests the company has more current assets than current liabilities, indicating that it is likely to meet its short-term obligations.

- Ratio = 1: Indicates current assets equal current liabilities. The company might pay off its short-term debts but has little margin for error.

- Ideal Ratio: While there is n specifically ideal current ratio, a ratio between 1.5 and 2.0 is usually deemed healthy, suggesting good liquidity without devoid of excessive idle assets. Furthermore, ideal current ratio may vary considerably by industry. Certain industries, such as supermarkets, probably operate lower ratios owing to high inventory turnover.

Quick Ratio

Quick ratio (the acid ratio) is a financial metric that evaluates a company’s ability to meet its short-term obligations using its most liquid assets. It is a more conventional measure of liquidity than the current ratio given that it excludes inventory and prepaid expenses, which be more complex to quickly convert into cash.

- The formula for calculating Quick Ratio = (Current Assets – Inventory) / Current Liabilities

OR

- Quick Ratio = (Cash & Cash Equivalents + Marketable Securities + Accounts Receivables) / Current Liabilities

Interpretation:

- A quick ratio of 1 or higher usually indicates a company can easily cover its short-term liabilities with its most liquid assets.

- A quick ratio 1 suggests the company could thrive to meet its immediate obligations.

- A higher quick ratio indicates greater liquidity and a more vital ability to manage short-term debts.

Debt to Equity (D/E)

Debt-to-equity ratio is a financial metric that is used to compare a company’s total liabilities to its total shareholders” equity. It suggests how much a company is using its debt versus equity to finance its assets. A higher D/E ratio indicates a greater reliance on debt, potentially rising financial risk.

- The formula for calculating Debt-to-Equity = Debt / Equity

Interpretation:

- High D/E Ratio: Suggests a company is heavily reliant on debt financing, which can be risky if the company faces financial problem.

- Low D/E Ratio: Indicates a company is using more equity financing and is less reliant on debt, potentially suggesting lower financial risk.

- Industry Variation: The ideal D/E ratio significantly varies across industries. Capital-intensive industries like manufacturing normally have higher ratios compared to service-based industries.

- Ideal Ratio: As a rule, a ratio below 1.0 generally deemed healthy, a ratio below 2.0 is usually considered as desirable.

Times Interest Earned (Interest Coverage Ratio)

Times Interest Earned (TIE) ratio, also known as the Interest Coverage Ratio, is a financial metric that suggests a company’s ability to meet its interest obligations on outstanding debt. It measures the number of times a company’s earnings before interest and taxes (EBIT) can cover its interest expenses. A high TIE ratio usually indicates that a company is in a stronger financial position and has stronger capacity to pay debts.

- The formula for calculating Times Interest Earned = EBIT (Operating Income) / Interest Expenses

Interpretation:

- Higher TIE Ratio: A higher TIE ratio is generally considered better, indicating a company has large earnings to cover its interest payments and less possibility to default on its debt.

- Lower TIE Ratio: A lower TIE indicates that a company may thrive to meet its interest obligations, potentially bringing about concerns about its financial health and ability to repay its debts. A lower ratio below 1.5 may create a cause for concern

- TIE Ratio Below 1: Suggests that a company is not earning enough profit to cover its interest expense, which can be a severe warning signal.

Return on Assets (ROA)

Return on Assets is a financial ratio that evaluates how efficiently a company utilizes its assets to generate profit. It suggests how efficiently a company is managing its assets to generate earnings. ROA generally suggests better performance, as it indicates the company is making more profit for each unit of money of assets its owns.

The formula for calculating Return on Assets = Net Income / Assets

Interpretation:

- A higher ROA suggests that a company is more efficient at utilizing its assets to generate profit.

- A lower ROA may suggest that a company is not utilizing its assets effectively or that it has involved in poor capital investments.

- It is significant to compare a company’s ROA to its historical ROA, and to the ROA of other companies in the same industry, as ROAs vary considerably between sectors.

Days Sales Outstanding

Days Sales Outstanding (DSO) is a financial metric that measures the average number of days it takes a company to collect payment after a sale has been made. It indicates how efficiently a company manage its accounts receivable and convert sales into cash. A lower DSO generally in indicates better cash flow and more effective and efficient collections.

- Formula for calculating DSO: (Accounts Receivable / Total Credit Sales) x Number of Days

Return on Equity (ROE)

Return on Equity is a financial ratio that evaluates a company’s profitability by indicating how much profit a company makes with the money shareholders have invested. ROE is a key metric of a company’s financial performance and its ability to earn profits from shareholders’ investments.

- Formula for calculating Return on Equity= Net Income / Equity

Interpretation:

- Higher ROE: Generally, a positive sign, indicating greater efficiency in using shareholder investments to generate profits.

- Lower ROE: May suggest that a company is not effectively using its equity to generate profits.

- Industry Context: ROE should be advisably compared within the same industry, as varied sectors have different profitability norms.

Return on Invested Capital (ROIC)

Return on Invested Capital is a financial indicator that measures how efficient a company generates profits from its invested capital. It suggests how efficiently a company is utilizing its capital to generate value, with a higher ROIC usually showing better performance.

- The formula for calculating Return on Invested Capital = EBIAT (Earnings Before Interest and After Tax) / Invested Capital = EBIT (1 – Tax Rate) / Debit + Equity

Or

ROIC = NOPAT / Invested Capital

Importance and Interpretation:

- Value Creation

ROIC is a key metric to evaluate whether a company is effectively creating value with its investments. When a company’s ROIC is more than its Weighted Average Cost of Capital (WACC), it is generating returns above its cost of capital, therefore, creating value.

- Efficiency

ROIC evaluates how efficiently a company utilizes its capital to generate profits. A higher ROIC indicates better capital allocation and operational efficiency.

- Industry Comparison

ROIC is used to compare the performance of companies within the same industry, highlighting which companies are more efficient at using capital.

- Long-Term Sustainability

A steadily high ROIC is usually considered as a positive sign for a company’s long-term sustainability, showing its ability to generate returns from its investments.

- Investment Decisions

Investors usually use ROIC as a key metric to measure the potential of a company’s investments and its aggregate value.

Self-Financing or Internal Growth Rate (IGR)

The internal Growth Rate is referred to as the maximum growth a company can attain using only its retained earnings, excluding external financing, such as a loan or equity. It is means of self-funded growth potential.

- Formula for calculating Internal Growth Rate (IGR) = ROA x Retained Earnings / 1- (ROA x Retained Earnings) >>> IGR = 1- (Dividends and Share Repurchases / Net Income)

Or

IGR = (Retained Earnings / Net Income) x (Net Income / Total Assets)

Advantages of Self-Financing (Internal Growth):

- Financial Control

More control over finances and decision-making, as there is no necessity to repay loans or depend on external investors.

- Lower Risk

Lower risk of financial distress or bankruptcy compared to depending largely on external debt.

- Sustain Values

A company can sustain its own values and culture while avoiding interference from stakeholders.

- Economies of Scale

Internal growth can result in lower average costs as production rises.

Disadvantages of Self-Financing (Internal Growth):

- Slower Growth

It is mostly likely that companies have limited resources which can slow down the pace of expansion and potentially constrains the company’s ability to effectively compete.

- Dependence on Forecasts

A company’s expansion or growth is usually dependent on accurate sales forecasts and the ability to effectively manage resources.

- Capital Limitations

A company may need considerable time to effectively accumulate enough retained earnings to fund larger projects.

Financial Ratio Calculations

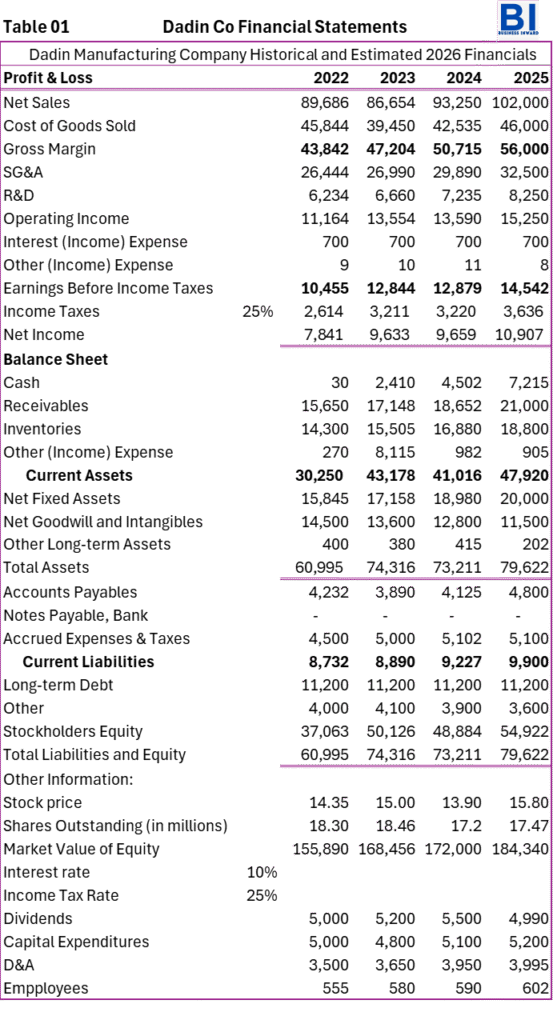

1. Compound Annual Growth Rates (CAGR) = [(Sales 2025 / Sales 2022)1/n] -1

= [(£102,000 / £89,686)1/3] – 1

= 4.4%

2. Days Sales Outstanding (DSO) = (Receivables x 365) / Sales

= (£21,000 x 365) / £102,000

= 75 days

3. Inventory Turnovers = Cost of Goods Sold (COGS) / Inventory

= £46,000 / £18,800

= 2.5 times

4. Days Sales in Inventory (DSI) = 365 / Inventory Turnovers

= 365 / 2.5

= 146 days

5. Operating Cash Cycle = DSO + DSI

= 75 + 146

= 221 days

6. Return on Invested Capital (ROIC) = EBIT (1 – Tax Rate) / Debt + Equity

= £15,250 (1 – 0.25) / (£11,200 + £54,922) = £11,437.50 / £66,17 = 17.3 %