Budget Planning and Forecasts

Budget planning is a process of creating or projecting a financial plan, a budget- that estimates and allocates future income and expenses over a particular period. This financial roadmap assists companies and individuals set objectives, allocate resources, control expenditure, and monitor the process.

Budget planning process entails analyzing historical financial data, forecasting future trends (conditions) setting financial goals, and then creating elaborated budget monitor to guide decision-making and attain financial stability.

Financial Projections

Short-term Projection

Short-term financial projections are financial estimates that predict financial plan and performance over a relatively short period, usually up to a year. They focus on operational activities and assist businesses manage day-to-day financial health. These projections typically include weekly, monthly, and quarterly financial breakdowns of projected revenues, expenses, cash flows, and other financial metrics.

Long-term Projection

Long-term financial projections are forecasts that estimate an organization’s financial plan and performance over an extended period, usually three to five, or more. These projections help businesses to make informed decisions related to capital budgeting, strategic planning, and allocation of resources.

Special Purpose Projection

Special purpose projections are tailored projections for specific projects or circumstances, typically hypothetical assumptions and scenarios. These projections are distinct from standard forecasts and used in situations in which general prediction of future financial performance is not sufficient.

Projection Evaluation

Organizations use different methods to evaluate potential projects, which include:

- Net Present Value (NPV): NPV is used to calculate present value of cash flows, discounted at cost of capital.

- Internal Rate of Return (IRR): IRR is used to determine the discount rate at which the NPV of a project equals zero.

- Payback Period: It is used to measure the time it takes for a project to recover its initial investment.

Budgeting Hypothetical Questions

Revenue

- How fast is the market growing?

- Is our market share expected to rise or decline? Why?

- Will we be able to rise prices?

- What new products will be brought into the market (by our organization and competitors)?

- What products will fail to meet sales expectation owing to product life cycles or the introduction of competitive product?

- What economic assumptions are contemplated in the plan?

- What is the general rate of inflation?

- What will happen to important costs such as key raw materials, labor, and related expenses such as employee health care.

- What rises to headcount will be needed to implement plan?

- What operating efficiencies and cost reduction can be achieved?

Asset and Investment Levels

- What level of receivables and inventories will be needed in the future?

- Will we require to rise capacity to achieve the planned sales levels?

Financing and Cost of Capital

- Will we require additional financial resources to implement the plan?

- Do we plan to change the mix of debt and equity in the capital structure?

- Is our business profile becoming more risky or less risky?

- What is likely to occur to interest rates over the plan horizon?

Overheads Budgeting Planning

Head of HR and Administration

- Annual salary is £65,000 per annum

- Pension contribution at 11.6% of annual salary: 11.6% x £65,000 = £7,540 per annum

- Private medical insurance: £2,800 per annum

- Performance bonus at 5% of annual salary: 5% x £65,000 = £3,250

- Lunch allowance is £3.20 x 262 days: £838.40

- Total remuneration: £65,000 + £7,540 + £2,800 + £838.40 = £78,428.40

Financial Controller

- Annual salary is £75,000 per annum

- Pension contribution at 11.6% of annual salary: 11.6% x 75,000 = £8,700 per annum

- private medical insurance is £2,800 per annum

- Performance bonus at 5% of annual salary: 5% x £75,000 = £3,250

- Lunch allowance is at £3.20 daily: £3.20 x 262 days = £838.40

- Total remuneration: £75,000 + £8,700 + £2,800 + £3,750 + £838.40 = £91,088.40

Variable Indirect Overheads

- Cleaning service cost is £14 per hour and 144 hours monthly: £14 x 144 hours = £2,016.00

- Monthly maintenance cost is at £25 per hour and 144 hours monthly: £25 x 144 hours = £3,600.00

- Average monthly electricity bill @ £1,900

- Average monthly water bill @ £340

- Average monthly toilet supplies @ £125

- Average cost of monthly maintenance and repairs @ £1,045

- Average cost monthly office supplies @ £443.58

- Total indirect overheads cost: £2,016 + £3,600 + £1,900 + £340 + £125 + £1,045 + £443.58 = £9,469.58

Budgets

Budgets are the most extensively used tools for planning and controlling organizations. They are a forward-looking plan that helps managers to be in a better position to capitalize on opportunities. In addition, budgets enable managers to anticipate risks and take steps to reduce or eliminate them.

Types of Budget

1. Rolling Budget

Rolling budget is referred to as a financial planning method where the budget is continually revised and updated by adding a new future period (month and quarter) as the current period ends, while dropping the earliest period. This brings about a budget that often looks ahead by a length of time, providing more flexibility and responsiveness to fluctuating circumstances benchmarked with traditional budgets.

2. Operating Budget

Operating budget is a financial plan that projects an organization’s expected revenues and expenses for a specific period, usually a month, quarter, or year. It constitutes a roadmap for how a business will allocate its resources to attain financial objectives.

Component of Operating Budget:

- Revenue: This includes all the income generated from a firm’s daily operations, for example sales of goods or service.

- Expenses: These include all costs (cost of goods sold & operating expenses) associated with operating a business.

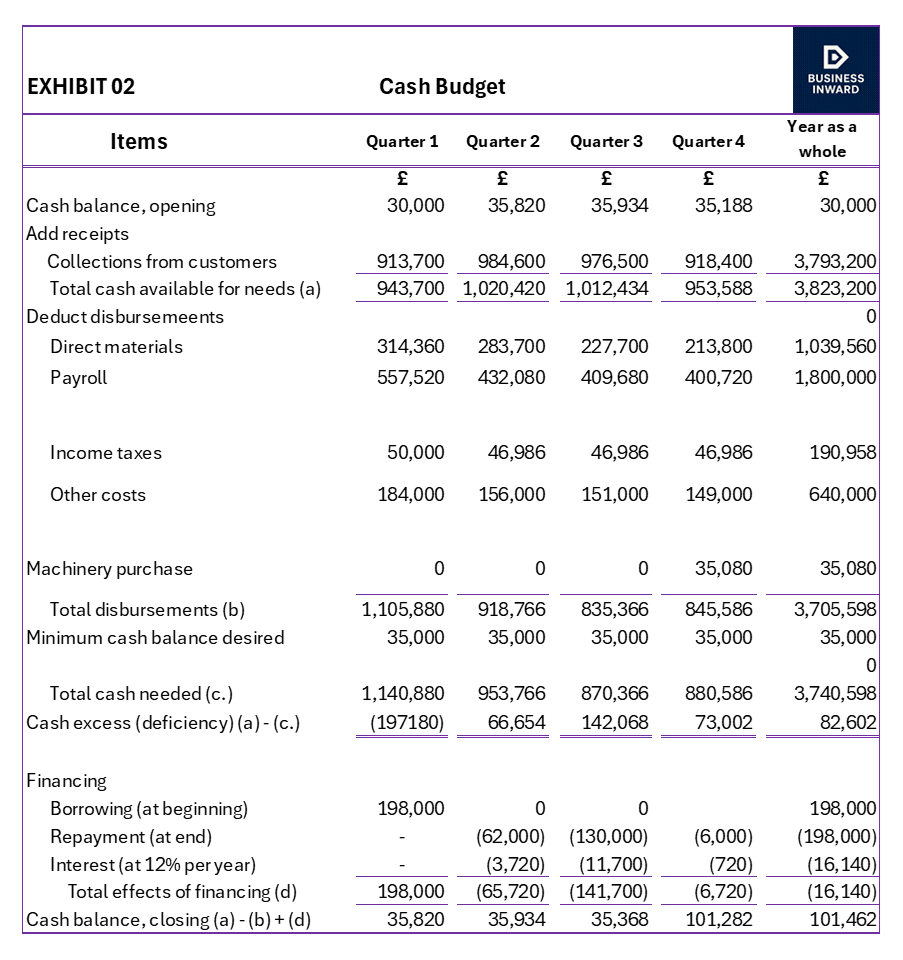

3. Cash Budget

A cash budget is a financial planning scheme that projects a business’s cash inflows and outflows over a particular period, enabling it to manage liquidity and ensure adequate funds for operations. It forecasts cash availability, recognizes potential shortages, and helps with proactive planning for borrowing or other financial reconciliations or adjustments.

Key Components and Benefits of cash Budget:

- Cash Receipts: Include all sources of cash flowing into business, for example sales revenue, loan proceeds, and sales of assets.

- Cash Disbursements: Include all cash flowing out of a business, such as operating expenses, capital expenditures, debt repayments, owner’s withdrawals.

- Beginning and Ending Cash Balances: The cash balance at the start of the period (previous period’s ending balance) and the projected cash balance at the end of the period).

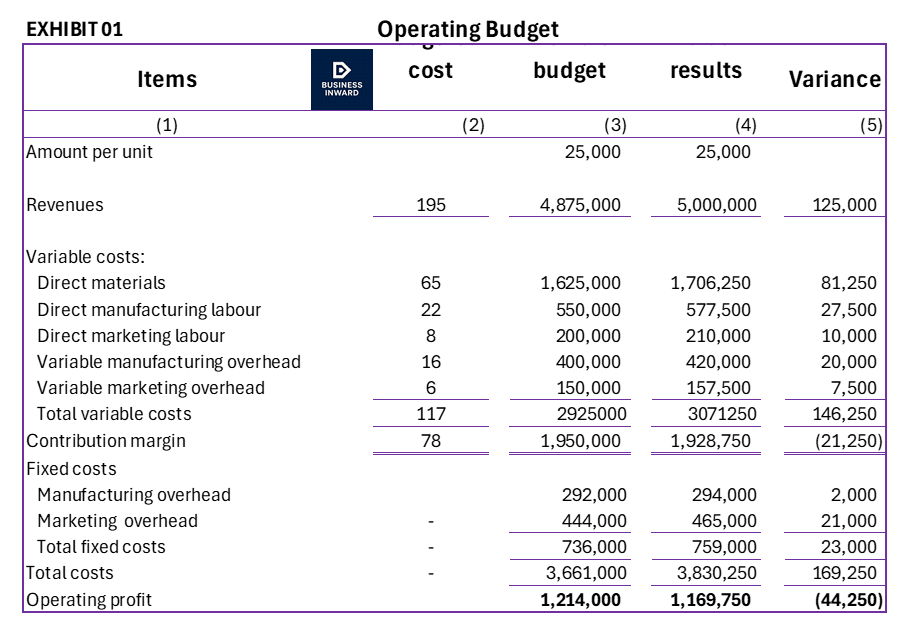

4. Flexible Budget

A flexible budget represents a financial plan that adjusts on changes in levels of activities, for example production output or sales volume. Unlike static budget, which remains constant or fixed, a flexible budget adapts to consider variations in costs and revenues, revealing a more realistic picture of a company’s financial performance. This adaptability enables businesses to make informed decisions and effectively resources in dynamic environment.

Variance

A variance is the difference between an actual result and a budgeted amount. The budgeted amount is the benchmark, which is the point of reference from which comparisons are made.

- Favourable and Unfavourable Variances

A variance is favourable if it its operating income increases relative to the budgeted standard. unfavourable variance decreases relative to the budegted standard.

Steps in Developing a Flexible Budget

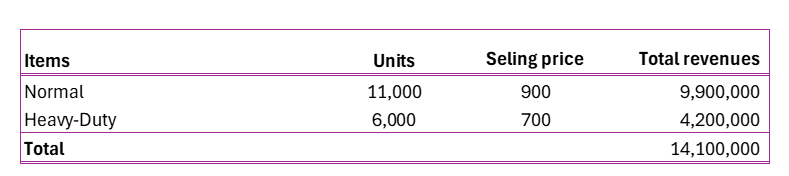

Step 1: Determine the budget selling price unit, the budgeted variable cost per unit, and the budgeted fixed cost.

Step 2: Production budget (in units):

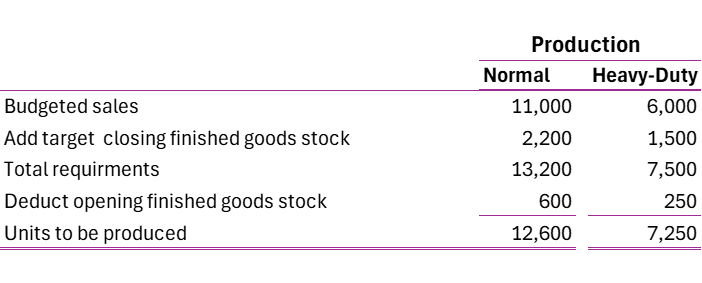

After revenues are budgeted, the production budget can be prepared. The total finished goods units to be produced depends on planned sales and expected changes in stock levels.

Schedule 1: Production budget (in units) for the year ending 31 December 2020:

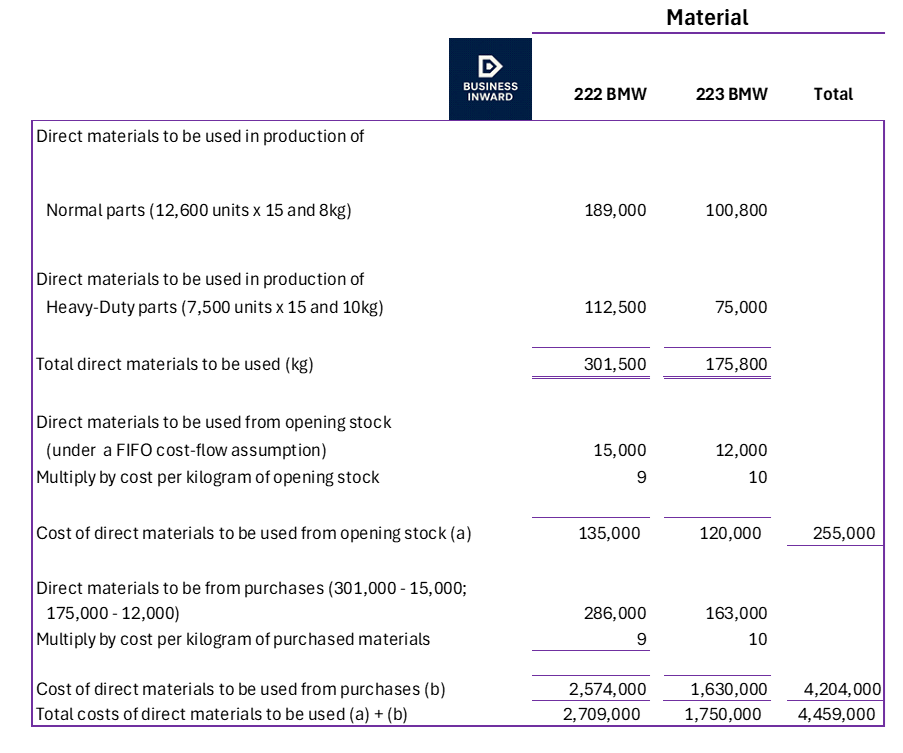

Step 3: Direct materials usage budget and direct materials purchases budget

Schedule 2: Direct materials usage budget in kilograms and pounds for the year ending 31 December 2020

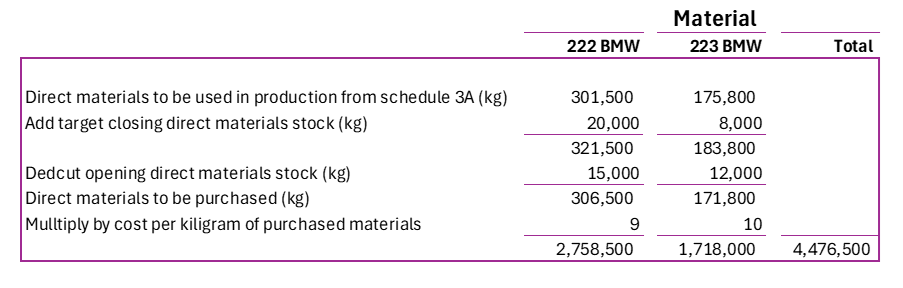

Schedule 2B: Compute the budget for direct materials purchase, which depends on the budgeted direct materials to be used, the opening stock of direct materials, and the target closing stock of direct materials:

Schedule 2B: Direct materials purchase Budget for the year ending 31 December 2020:

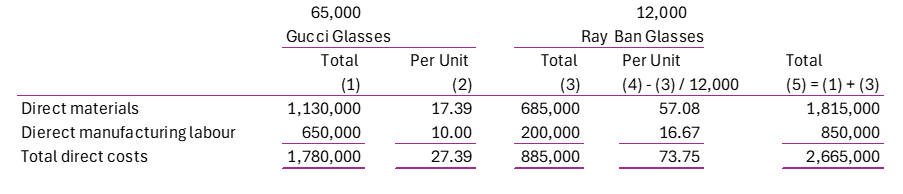

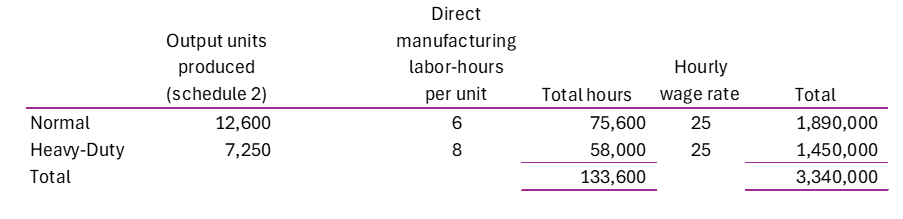

Step 4: Direct manufacturing labor budget. These costs depend on wage rates, production methods and hiring plans.

Schedule 3: Direct manufacturing labor budget for the year ending 31 December 202:

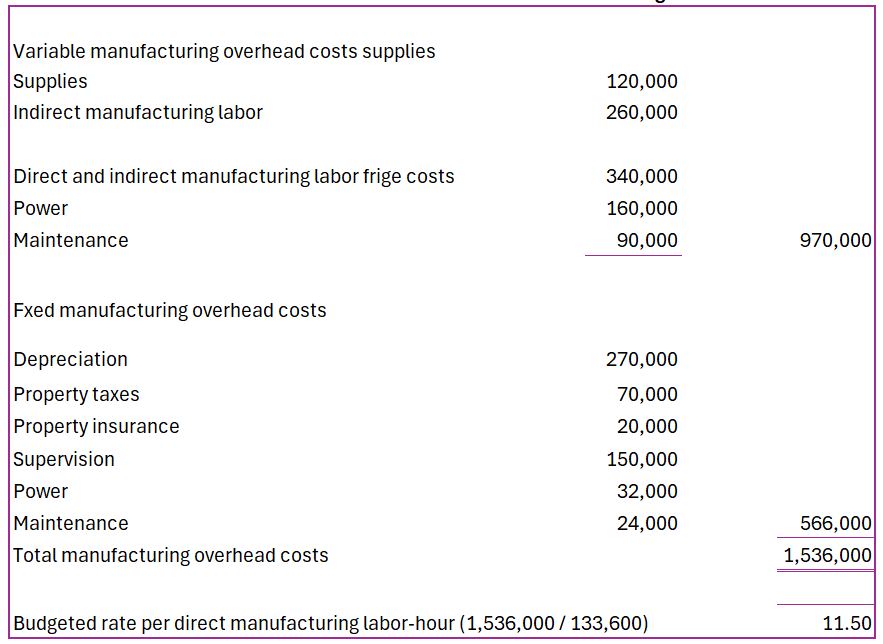

Step 5: Manufacturing overhead budget. The total costs depend on how individual overheads costs vary with the assumed cost driver, direct manufacturing labor-hours. The specific variable-and fixed-cost categories may be obtained.

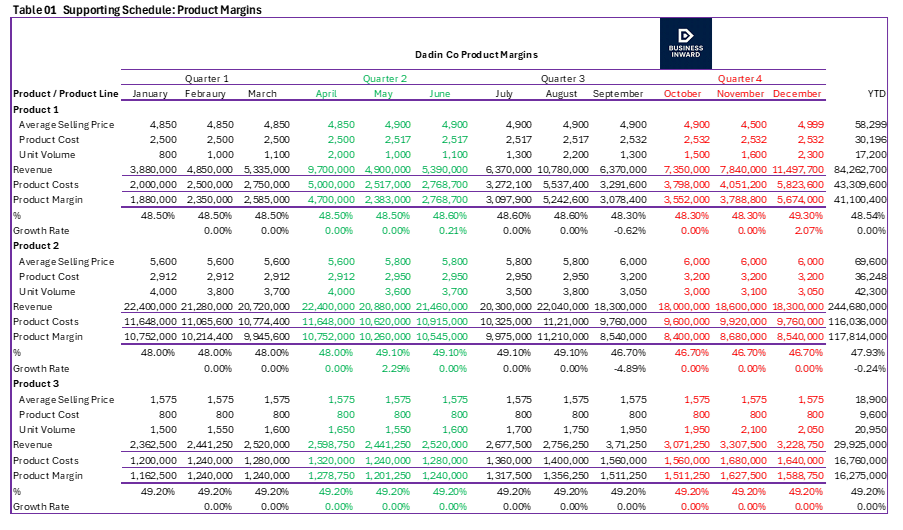

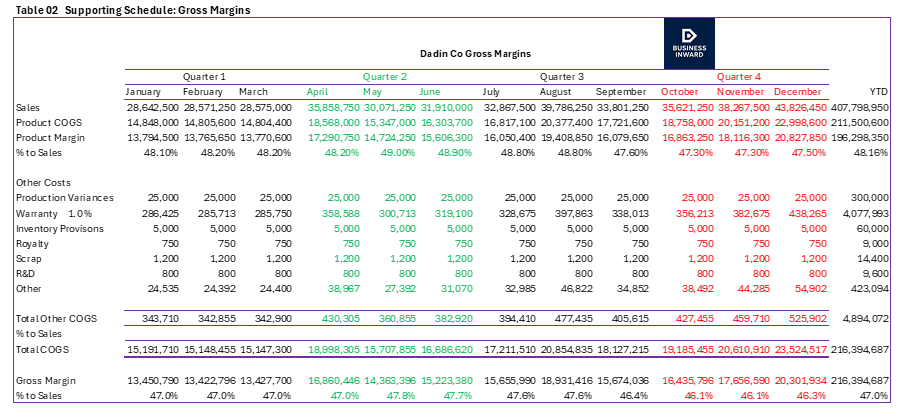

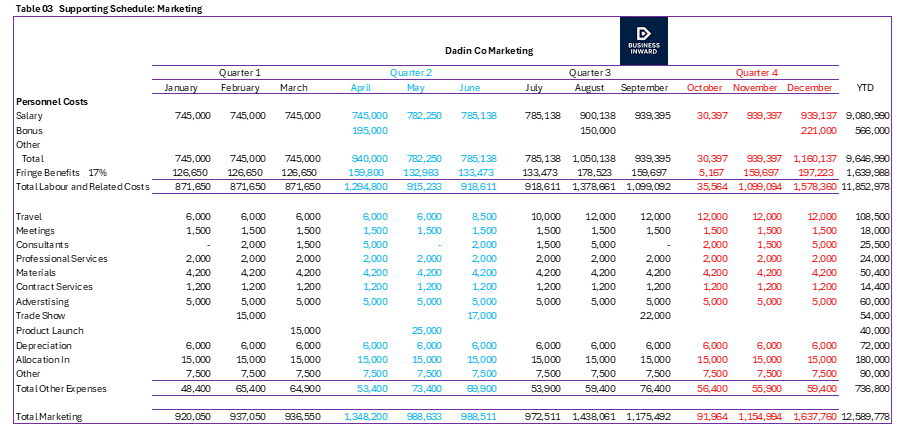

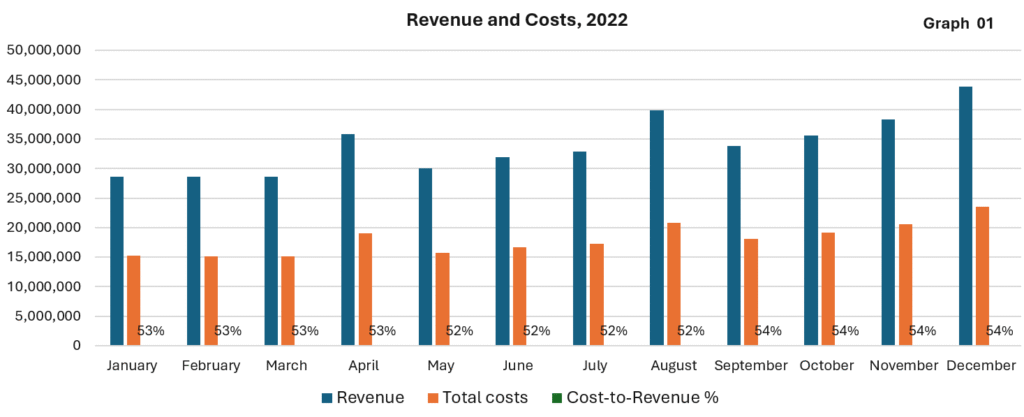

Budget & Analysis Spreadsheets