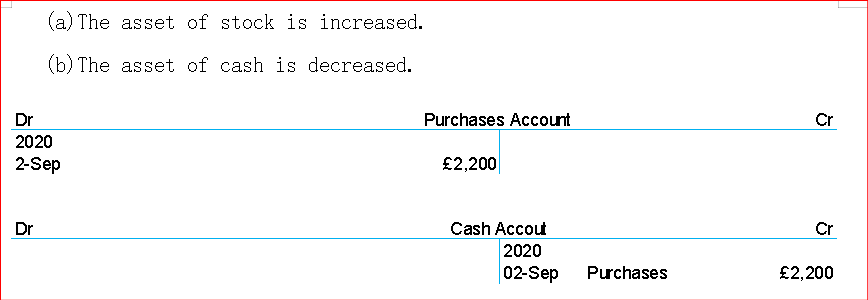

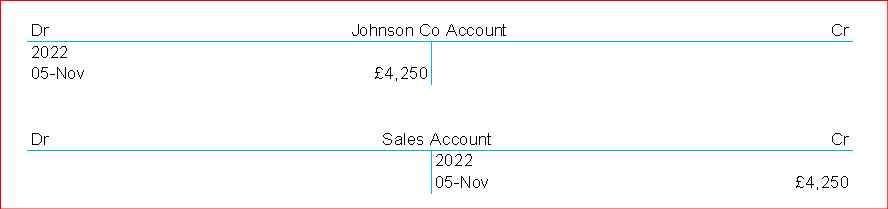

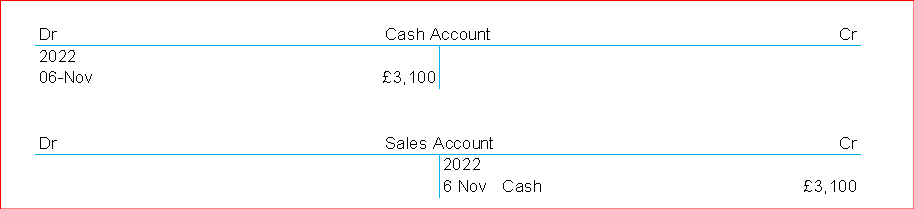

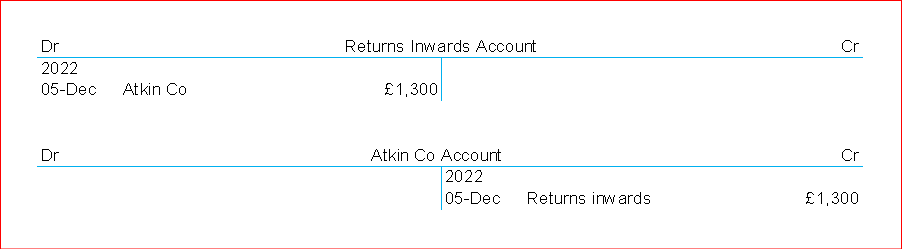

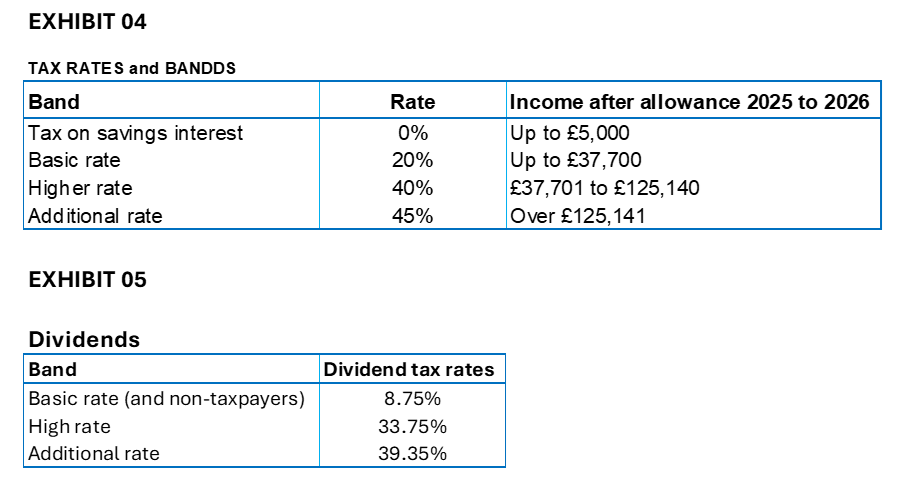

In 2025, the dividend allowance is £500.

If John earns £4,000 in dividends and earns £27,860 in wages in 2024/2025 tax year. This gives a total income of £31,860. John is entitled to personal allowance of £12,570, which is taken off his total income to result in a taxable income of £19,290.

- Thus, 20% tax on £15,290 wages gives £3,058 tax payable.

- No tax on £500 dividends, because of dividend allowance.

- 75% tax on £3,500 results in £308 tax payable.

VAT RETURN

VAT Return is a form that businesses registered for Value Added Tax (VAT) in many countries, which must be completed and submitted to the tax authority at regular intervals, usually every quarter. The VAT-return form entails details of the business’ sales and purchases during a specific period and indicates the amount of VAT charged and paid.

VAT INPUT and VAT OUTPUT

Input VAT is the VAT paid by a business on its purchases of goods and services, while Output VAT is the VAT charged by a business on the sales of goods and services.

At Business Inward, we render services of VAT-return preparation and filing to our customers.

National Insurance contributions (NICs) in the UK

An income earner aged 16 or above pays NICs.

- An employee who earns more than £242 weekly from a job pays NICs.

- A self-employed person who makes a profit of more than £12,570 yearly pays NICs.

An income earner does not qualify to pay National Insurance, but still qualifies for certain benefits and the State Pension, if she/he is either:

- An employee earning from £125 to £242 weekly.

- A self-employed person who earns a profit of £6,845 or more yearly.

Whatever contributions made under this context are treated as having been paid to protect your National Insurance record.

Ultimately, there are various classes of NICs in the United Kingdom. Yearly, the Tax Authority usually changes the amount of contributions under the different classes.

The information above is a brief overview of NICs.

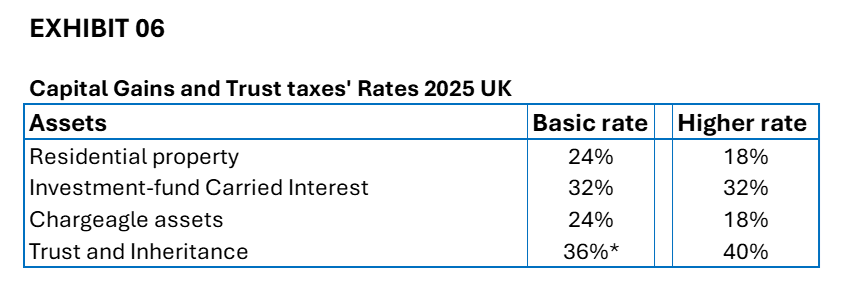

Capital Gains Tax and Allowances

Capital Gains Tax is a tax paid on the profit when you sell or dispose of assets that is appreciated in value. It is the gain you make after disposing of an asset that is taxed, not the amount of money you receive.

You only must pay Capital Gains Tax on your aggregate gains above your tax-free allowance (known as ‘the Annual Exempt Amount).

The capital Gains tax-free allowance is:

You may also be able to reduce your tax bill by deducting losses or claiming reliefs, depending on the asset being disposed of.

For instance, if you purchased machinery for £10,000 and sold it later for £24,000, you have earned a gain of £14,000.