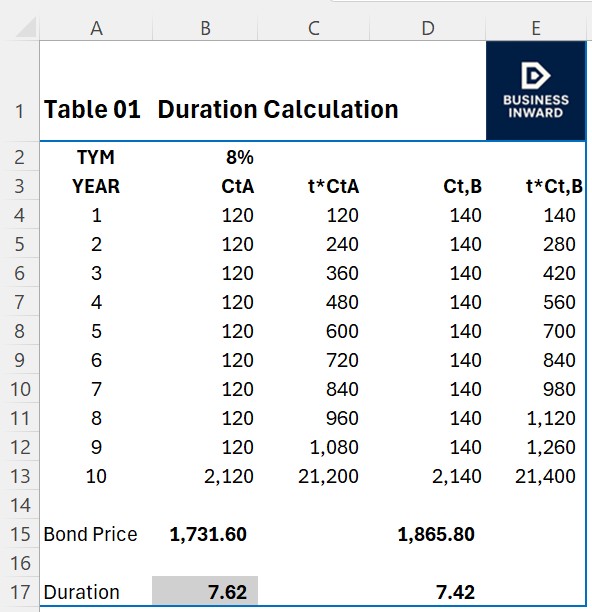

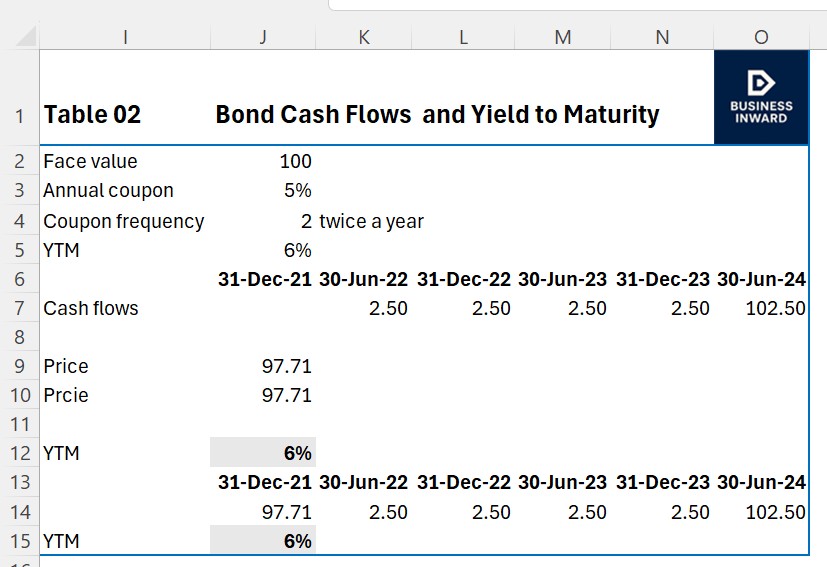

Bond Price & Duration

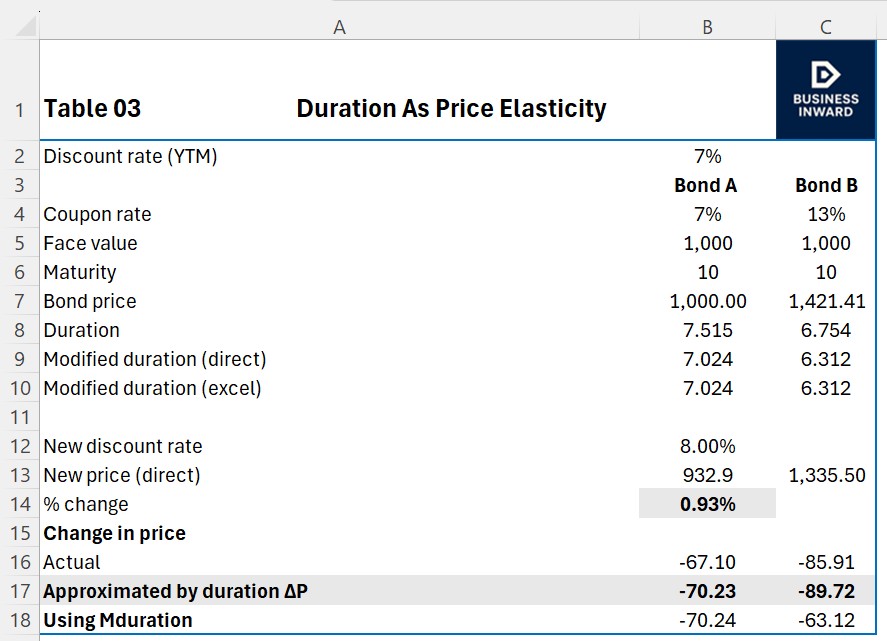

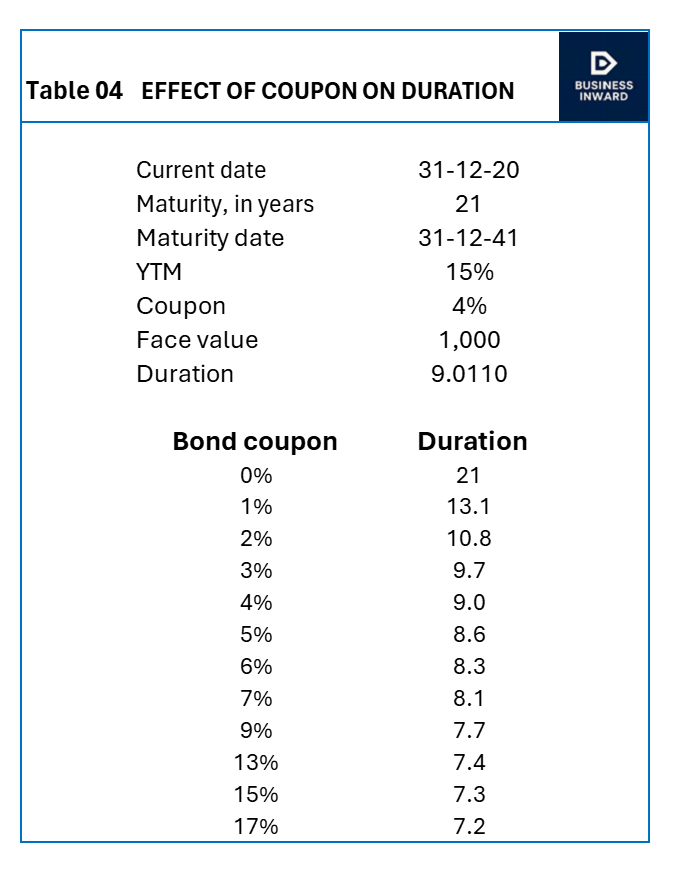

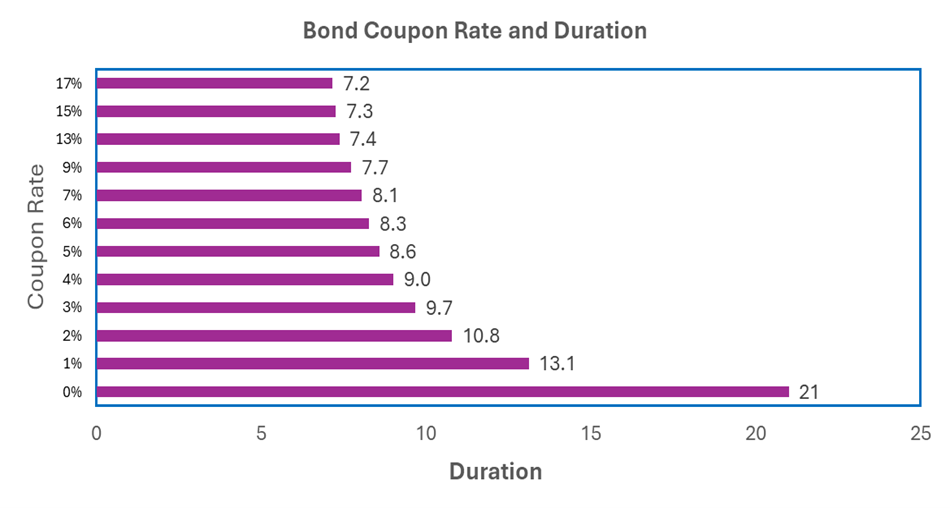

Duration As Price Elasticity & Effect of Coupon on Duration

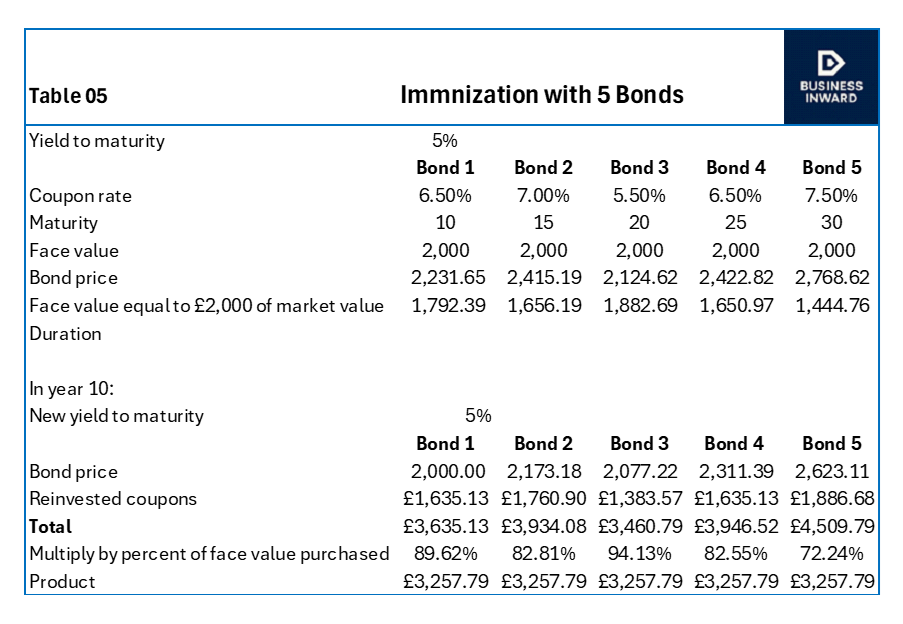

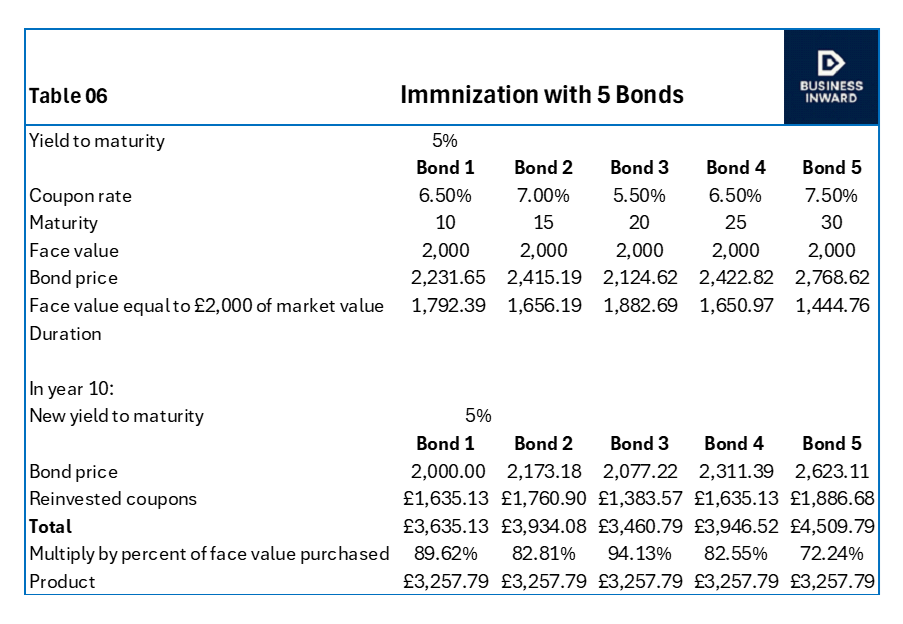

Bond Immunization

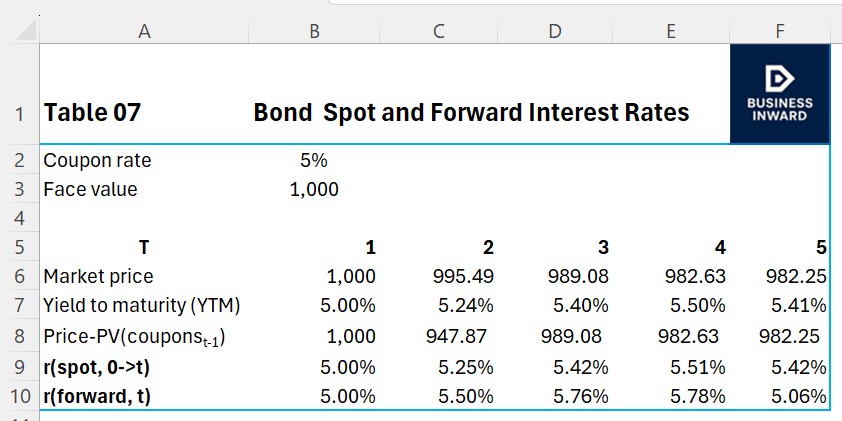

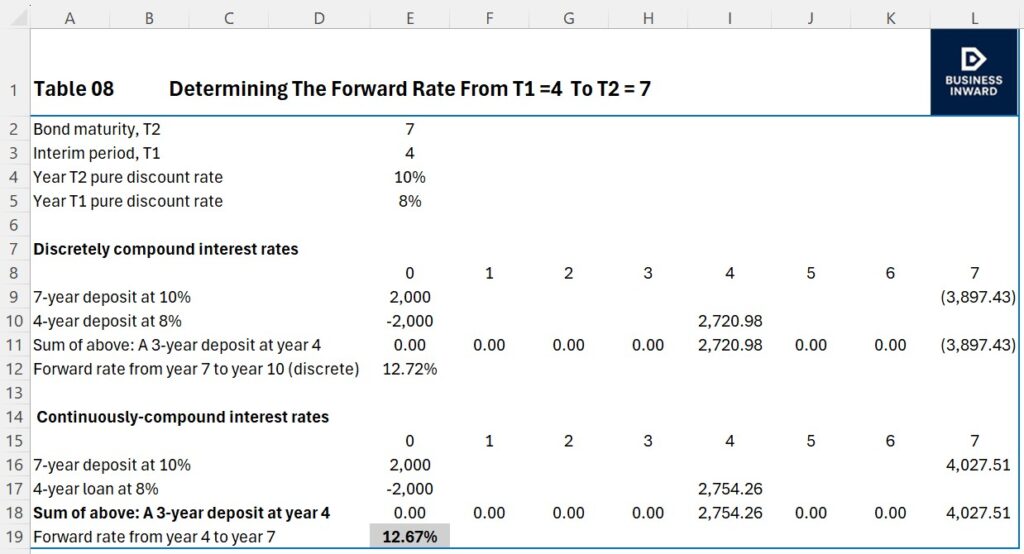

Spot and Forward Interest Rates