Bad Debts and Provisions for Doubtful Debts

Bad Debts:

If a company realizes that it is impossible to collect a debt, then that debt should be written off as a bad debt. This could occur if the debtor encounters a loss in the business, or perhaps even gone bankrupt and is thus unable to pay the debt. Therefore, a bad debt becomes an expense on the company that is owed the money.

Example:

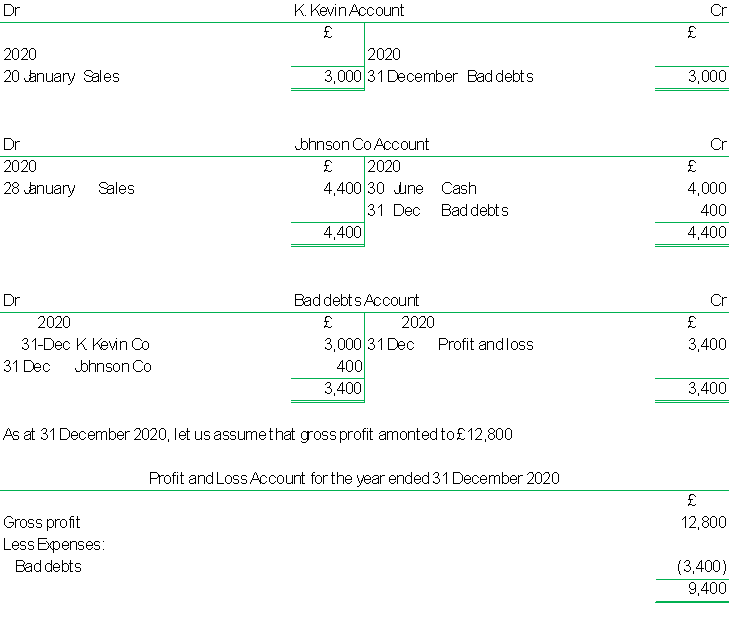

Dadin Co sold £3,000 goods to K. Kevin Co on 20 January 2020, and K. Kevin Co became bankrupt.

On 28 January 2020, Dadin Co sold £4,400 goods to Johnson Co. Johnson managed to pay £4000 on 30 June 2020, but it became obvious that he would never be able to pay the final £400.

At 31 December 2020, when Dadin Co is drawing up final accounts, it decided to write these off as bad debts. The account entries are shown below:

Provision for doubtful Debts:

Provision for doubtful Debts:

A provision for doubtful debts, also known as an allowance for doubtful accounts or bad debt provision, is an accounting value of the portion of a firm’s accounts receivable that is likely uncollectible. It is a contra asset, which means it reduces the total value of accounts receivable on the balance sheet, and results in accurate representation of the net realizable value of accounts receivable (the collectible amount).

Accounting entries for provisions for doubtful debts:

- Profit and loss account (with the amount of provision): (Dr)

- Provision for doubtful debts account: (Cr)

Example:

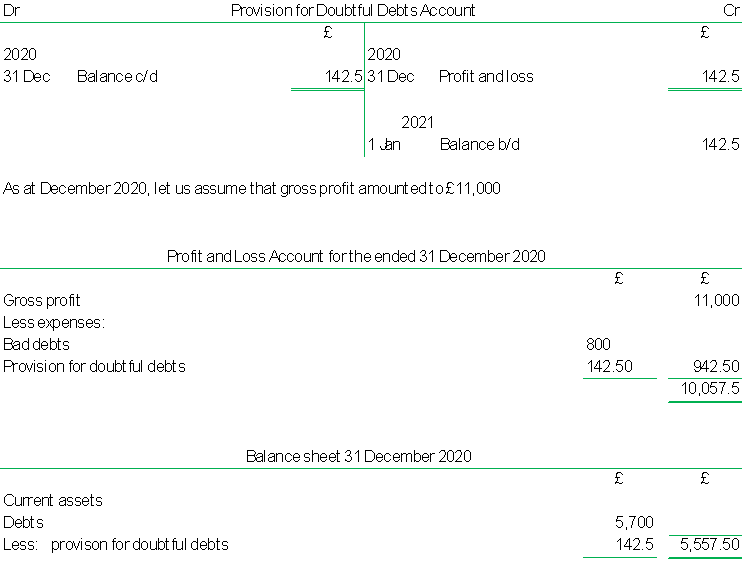

As at 31 December 2020, the debtors’ value for K. Kevin Co amounted to £5,700 after writing off £800 of definite bad debts. It is valued that 2.5 percent of debts (i.e., £5,700 x 2.5% = £142.50) will prove to be bad debts, and it is decided to make a provision for the bad debts.

The accounts would appear as follows:

The double entry for the increasing provision:

- Profit and loss account: (Dr)

- Provision for doubtful debts account: (Cr)

The double entry for reducing the provision:

- Provision for doubtful debts account: (Dr)

- Profit and loss account: (Cr)

The double entry for Bad debt recovered:

- Debtor’s account: (Dr)

- Bad debts recovered account: (Cr)