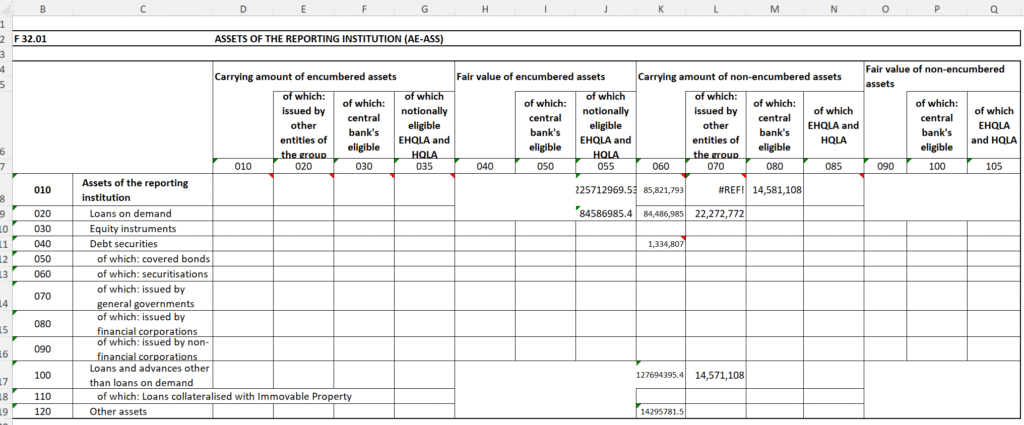

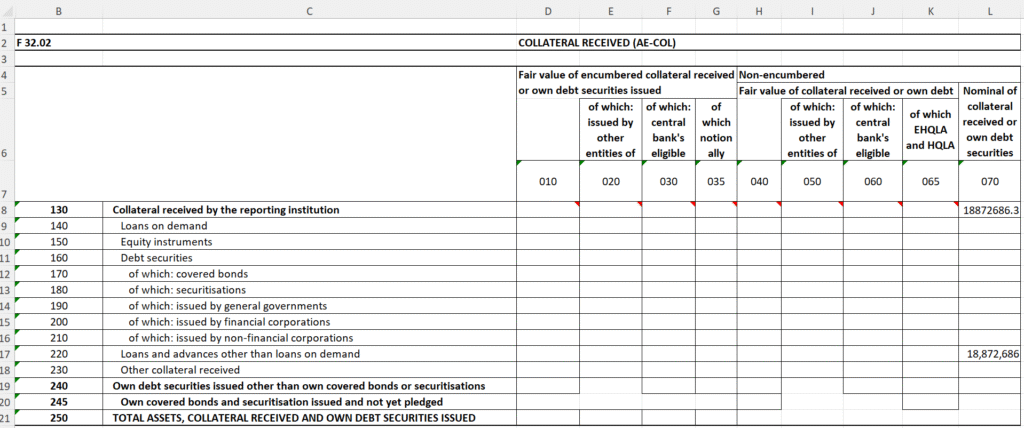

Features of asset encumbrance reporting

Examples of Encumbered Assets

Asset Encumbrance Spreadsheets