Anti-Money Laundering (AML)

AML is the set of laws, regulations, and procedural frameworks used to preclude criminals from disguising unlawfully obtained funds as legal income. It involves financial institutions and other regulated entities scrutinizing customer identities, monitoring transactions for suspicious activities, including reporting it to authorities. AML regulatory framework is instituted to combat crimes, such as drug trafficking, terrorism financing, and evasion of tax.

In the UK, key offences under Proceeds of Crime Act 2002 (POCA) entail concealing, disguising, or converting criminal property, including, using, or possessing criminal property. In addition, the Sanctions and Anti-Money Laundering Act 2018 (SAMLA) was specifically enacted to sanctions prevention of money laundering and terrorist financing.

Updated 30 August, 2025.

Features of Anti-Money Laundering (AML) Legislation

- Legislation: In the UK, principal laws entail SAMLA 2018 and the Proceeds of Crime Act 2002 (POCA). POCA specifically criminalizes acts, namely concealing, disguising, or using criminal property.

- Regulations: Regulations, such as the UK’s Money Laundering Regulations 2017 (MLRs) is saddled with day-to-day responsibilities on corporate entities, especially professional services, such as law firms to adhere to AML rules.

- Risk-based approach: Businesses must evaluate the risk of money laundering linked with their activities and carry out controls in proportion to that risk.

- Customer due diligence (CDD): Companies must identify and verify the identity of their clients and comprehend the sources of their funds and wealth.

- Internal controls: Firms require policies, controls, and monitoring systems to manage risks. This entails training staff and conducting background checks.

- Suspicious Activity Reporting (SARs): Business entities have a legal obligation to report any suspicious financial activity to the appropriate authorities.

- Sanctions screening: Under the SAMLA 2018, organizations must screen their activities against sanctions lists to preclude transactions with designated persons or entities.

Anti-Terrorism ACT

Anti-terrorism is referred to as strategies, laws, policy actions adopted to counter terrorism, which aims to prevent, detect, and react to terrorist attacks. The UK’s strategy, CONCEPTS, is established on four pillars: (i) Prevent (halt people from becoming terrorists), (ii) Pursue (halt attacks from happening), (iii) Protect (harden targets), and (iv) Prepare (minimize the impact of an attack). In the UK, suspicious activity of terrorism can be reported Counter Terrorism Policing at gov.uk/ACT, or by calling the confidential hotline on 0800 789 321, for immediate risk, call 999.

Anti-Terrorism Act

Anti-terrorism act can refer to many laws, encompassing the recent Terrorism (Protection of Premises) Act 2025 (Martyn’s Law), which necessitates venues to prepare for terrorist attacks, and earlier Terrorism Act 200 and the Anti-terrorism, Crime and Security Act 2001, which confer power for police and security services, sentencing, including asset freezing. The Acts aim to countering and responding to terrorism through powers to disrupt, monitor, and react to attacks and funding.

- Terrorism (Protection of Premises) Act 2025 (Martyn’s Law): Aims to improve public safety by requiring venues and events to have a plan to respond to a terrorist attack and take steps to reduce vulnerability.

- Counter-Terrorism and Sentencing Act 2021: Foster the management of terrorist offenders, and the related Crime Bill will add breaching foreign travel restriction orders to this regime for consistency.

- Counter-Terrorism and Border Security Act 2019: Introduced new offences, such as making it an offence to express opinions that support a proscribed organization.

Previous landmark UK anti-terrorism legislation:

- Counter-Terrorism and Security Act 2015: Aims to disrupt travel for terrorist activity, improve the ability of agencies to monitor threats, and combat terrorist ideology.

- Terrorism act 2006: Makes provision for offences related to terrorism and amends existing legislation.

- Anti-Terrorism, Crime and Security Act 2001: Enacted after 9/11, it was a principal piece of legislation that introduced powers for asset freezing, information sharing, and updated immigration procedures.

- Terrorism Act 2000: Consolidated previous law and provided police new powers of arrest, search, and seizure related to terrorism.

Economic Impact of Anti-money Laundering

Anti-money laundering (AML) has both positive and negative economic impacts, encompassing costs for businesses and potential negative effects on GDP per capita, but it also provides advantages, such as enhanced financial stability, investor confidence, and fair competition by disrupting criminal activity. The economic landscape is shaped by the trade-offs between AML’s preventative measures and its compliance burdens.

Negative Economic Impacts

- High compliance costs for businesses: Financial institutions incur substantial costs for AML compliance, namely staffing, technology, and training. These costs can be passed on to customers.

- Reduced access to financial services: Banks occasionally de-risk by closing accounts of customers who present a higher risk, even if they are innocent, because the cost of full investigation would outweigh the value of their business.

- Potential negative correlation with GDP per capita: Certain researches have found that higher Basel AML scores are associated with lower GDP per capita, possibly owing to the way regulations affect market imperfections.

- Increased remittance costs: AML regulations can rise the cost of receiving remittances, specifically when combined with other factors.

Positive Economic Impacts

- Increased economic stability: By disrupting criminal finance and money laundering, AML measures help keep the integrity of financial markets and ensure resources are allocated and distributed fairly.

- Protection of honest businesses: Money laundering can distort markets by allowing criminal funds to enter legitimate business sectors, making it harder for honest businesses to compete. AML regulations protect against this, supporting to prevent job losses and business closures.

- Enhanced investor confidence: Poor AML performance can undermine investor confidence and deter foreign investment. Strong AML frameworks, conversely, can improve investor confidence and attract legitimate investment.

- Reduced funding for illegal activities: Effective AML controls help mitigate the funding available for terrorism, organized crime, and other illegal activities.

- Benefits of a stronger global economy: Combating money laundering helps create a more stable and transparent global economy, spurring international cooperation and compliance to standards.

Firm-Wide Risk Assessment (FWRA) for Anti-Money Laundering (AML)

Firm-wide risk assessment (FWRA) for anti-money laundering (AML) is a written document that identifies and evaluates the risks of money laundering a business encounters, and elaborates how these risks will be reduced. It should assess risk factors related to clients, geographic areas, products and services, transactions, and delivery channels to establish an effective AML policy. The FWRA must be regularly reviewed and updated to remain effective.

Key steps for an AML Firm-Wide Risk Assessment

- Identify and assess risks: Analyze the firm’s exposure to money laundering by considering various risk factors:

- Clients: Look at client demographics, whether they are Politically Exposed Persons (PEPs), and the complexity of ownership structures.

- Geographic Areas: Evaluate risks associated with countries or regions where the firm operates, or where clients are based.

- Products and Services: assess the risk from specific services offered, such as conveyancing, tax advice, or the use of client bank accounts.

- Transactions: Consider the size, frequency, and complexity of transactions.

- Delivery Channels: Analyze risks associated with how services are delivered, like online, in-person, or remote.

- Mitigate risks: Design and implement policies, procedures, and controls to manage and reduce the impact of the identified risks. The FWRA should inform the level of customer due diligence (CDD) and monitoring required for clients and matters.

- Maintain and review: The FWRA should be a living document that is regularly reviewed and updated. Review it proactively (e.g., annually) and reactively in response to significant changes, such as new business areas, legislative updates, or changes in control measures.

- Record and document: Keep a record of the risk assessment and the steps taken to prepare it, and be prepared to provide it to the supervisory authority upon request.

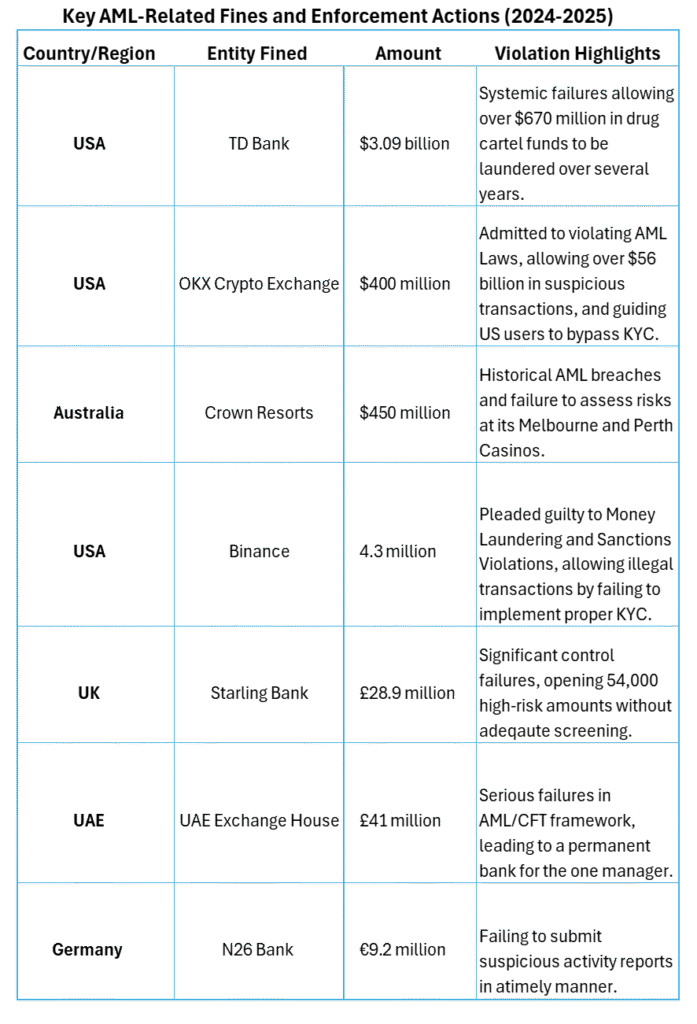

Fights and Fines against Anti-Money Laundering by Countries