Budgets and Responsibility Accounting

Budgets

Budgets are one of the most extensively used tools for planning and controlling organizations. Budgeting systems turn managers’ perspective forward. A forward-looking perspective helps managers to be in a better position to capitalize on opportunities. In addition, budgets enable managers to anticipate risks and take steps to reduce or eliminate them.

Budgets can compute the planned financial effects of activities focused on continuing improvement, and cost reduction, including assessing the performance of managers or the business areas.

Numerous organizations adopt the following budget cycle:

- Planning the performance of the organization as well as its subunits, and the entire management team consents upon what is expected.

- Providing a point of reference, a set of specific or tailored expectations against which actual results can be contrasted.

- Examining variations from plans. If essential, corrective measure follows examination.

- Planning again, reviewing feedback and altered conditions.

Roles of Budgets

Budgets are a principal characteristic of management control systems. Current thinking regarding budgetary control systems postulates two opposite views. The first view that supports incremental improvements to budgetary procedures, in terms of associating such procedures more closely to operational requirements and planning systems and upscaling the frequency of budget revisions and the execution of rolling budgets. The second view advocates the desertion of budgetary control and its replacement with optional techniques to ensure organizations become more adaptive and agile.

Strategy and Plans

Budgeting is most significant when done as an integral aspect of organization’s strategic analysis. Strategy can be viewed as expressing how an organization matches its own capabilities with the opportunities in the marketplace to achieve its overall goals.

Strategic analysis outlines both long-term and short-term planning. Subsequently, these plans result in the formation of budgets. Budgets give feedback to managers about the possible impacts of their strategic plans.

Coordination and Communication

Coordination is the harmonizing and balancing of all characteristics of production or service and all the departments and business functions so that organization can meet its goals. Communication is getting those goals understood and consented by all departments and functions.

1. Rolling Budget

Rolling budget is referred to as a financial planning method where the budget is continually revised and updated by adding a new future period (month and quarter) as the current period ends, while dropping the earliest period. This brings about a budget that often looks ahead by a fixed length of time, providing more flexibility and responsiveness to fluctuating circumstances benchmarked with traditional budgets.

2. Operating Budget

Operating budget is a financial plan that projects an organization’s expected revenues and expenses for a specific period, usually a month, quarter, or year. It constitutes a roadmap for how a business will allocate its resources to attain its financial objectives.

Key Components of Operating Budget:

- Revenue: This encompasses all the income generated from a firm’s daily operations, for example sales of goods or services.

- Expenses: This includes all costs associated with operating the business, encompassing:

- Cost of Goods Sold (COGS): Direct costs associated with producing goods or providing services.

- Operating Expenses: Indirect costs, such as rent, utilities, salaries, marketing, and administrative costs.

Steps in Preparing an Operating Budget:

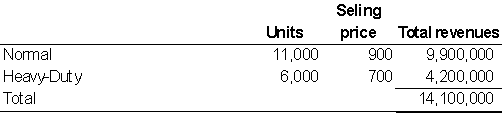

Step1: Revenue Budget for the year ending 31 December 2020.

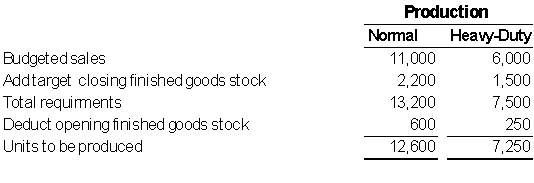

Step 2: Production budget [in units]

After revenues are budgeted, the production budget can be prepared. The total finished goods units to be produced depends on planned sales and expected changes in stock levels.

Schedule 2: Production budget (in units) for the year ending 31 December 2020

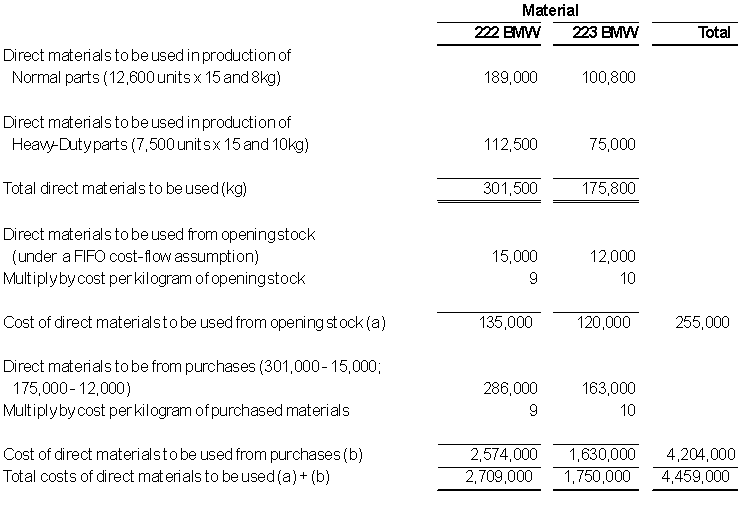

Step 3: Direct materials usage budget and direct materials purchases budget

Schedule 3A: Direct materials usage budget in kilograms and pounds for the year ending 31 December 2020

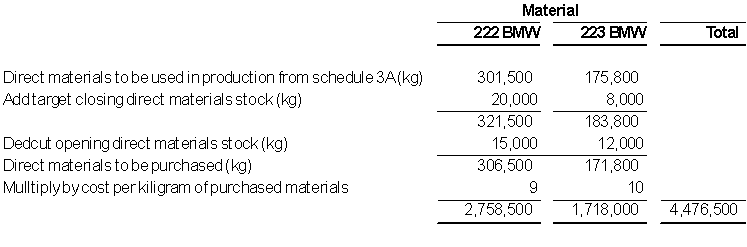

Schedule 3B computes the budget for direct materials purchases, which depends on the budgeted direct materials to be used, the opening stock of direct materials, and the target closing stock of direct materials:

Schedule 3B: Direct materials purchases budget for the year ending 31 December 2020

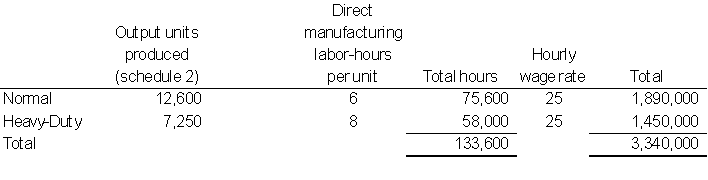

Step 4: Direct manufacturing labor budget. These costs depend on wage rates, production methods and hiring plans.

Schedule 4: Direct manufacturing labor budget for the year ending 31 December 2020

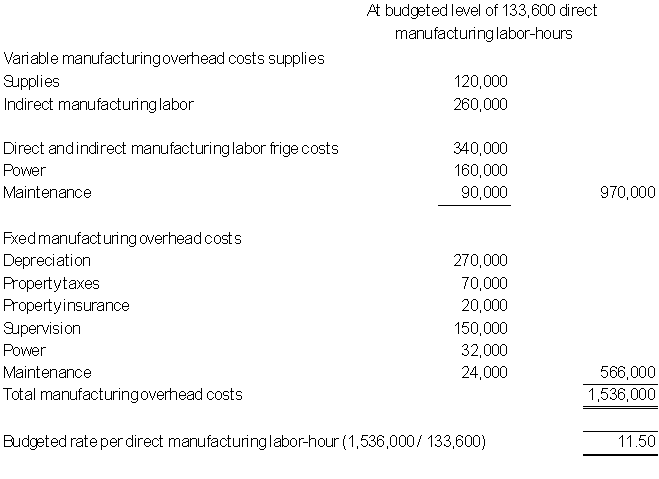

Step 5: Manufacturing overhead budget. The total costs depend on how individual overheads costs vary with the assumed cost driver, direct manufacturing labor-hours. The specific variable-and fixed-cost categories may be obtained.

Schedule 5: Manufacturing overhead budget for the year ending 31 December 2020

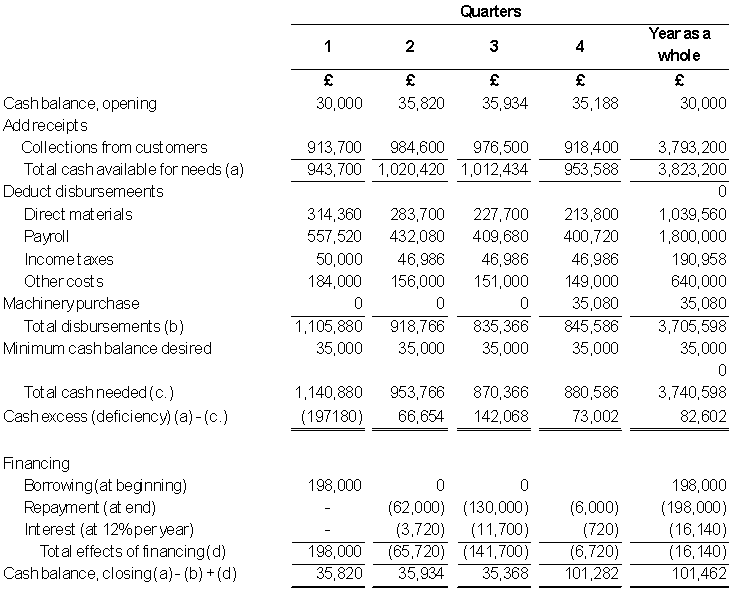

3. Cash Budget

A cash budget is a financial planning scheme that projects a business’ s cash inflows and outflows over a particular period, enabling it to manage liquidity and ensure adequate funds for operations. It forecasts cash availability, recognizes potential shortages, and helps with proactive planning for borrowing or other financial reconciliations or adjustments.

Key components and Benefits of Cash Budget:

- Cash Receipts: Encompasses all sources of cash flowing into a business, for example sales revenue, loan proceeds, and sales of assets.

- Cash Disbursements: Includes all cash flowing out of a business, such as operating expenses, capital expenditures, debt repayments, and owner’s withdrawals.

- Beginning and Ending Cash Balances: The cash balance at the start of the period (previous period’s ending balance) and the projected cash balance at the end of the period).

- Cash Excess or Shortfall: The difference between total cash inflows and outflows to ascertain if a business has a surplus or requires additional financing.

4. Flexible Budget

A flexible budget represents a financial plan that adjusts on changes in levels of activities, for example production output or sales volume. Unlike static budget, which remains constant or fixed, a flexible budget adapts to consider variations in costs and revenues, revealing a more realistic picture of a company’s financial performance. This adaptability enables businesses to make informed decisions and effectively manage resources in dynamic environment.

- Variance and Benchmark

A variance is the difference between an actual result and a budgeted amount. The budgeted amount is the benchmark; it is the point of reference from which comparisons are made.

- Standard and Management by Exception

A standard is a prudently predetermined amount; it is often expressed on a per unit basis. There is a dividing line between a budgeted amount and standard amount. Management by exception is the practice of focusing on areas not operating as expected or foreseen, and giving less attention to areas operating is required.

- Favourable and Unfavourable Variances

A variance is favourable if its operating income increases relative to the budgeted standard. Unfavourable variance decreases relative to the budgeted standard.

Static-budgeted variance of operating profit = Actual results – Static-budgeted amount

Steps in Developing a Flexible Budget

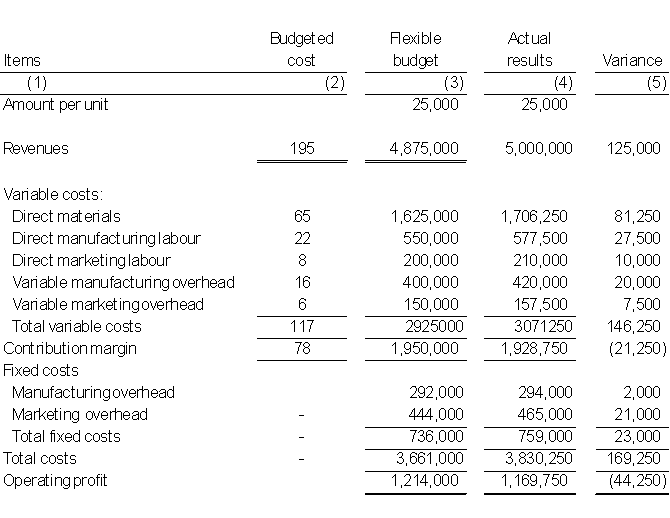

Step 1: Determine the budgeted selling price unit, the budgeted variable costs per unit, and the budgeted fixed costs.

Step 2: Determine the actual quantity of the revenue driver. Dadin Co’s revenue driver is the number of units sold.

Step 3: Determine the flexible budget for revenue based on the budgeted unit revenue and the actual quantity of the revenue driver.

Flexible-budgeted revenues = £195 x 25,000

= £4,875,000

Step 4: Determine the actual quantity of the cost driver(s). Dadin Co’s cost driver for manufacturing costs is units produced. The cost driver for the marketing costs is units sold. Dadin Co produced and sold 25,000 shoes.

Step 5: Determine the flexible budget for costs based on the budgeted unit variable costs and fixed costs and the actual quantity of the cost driver(s).

Sales-Volume Variances

Flexible-budget Variances

- Price Variance and Efficiency Variance

A price variance is the difference between the actual price and the budgeted price multiplied by the actual quantity of input in question (e.g., direct materials purchased or used). Price variances are sometimes referred to as input-price variance or rate variances (especially when variances are for direct labor). An efficiency variance is the difference between the actual quantity of input used and the budgeted quantity of input that should have been used, multiplied by the budgeted price. Efficiency variances are sometimes called input-efficiency variances or usage variances.

Price variance = (Actual price of input – Budgeted price of input) x Actual quantity of input