FINANCIAL REPORTING

Measuring and Reporting Financial Position

The principal financial accounting statements aim to present a picture of financial position and performance of a business. To attain this, a business’s accounting system will typically produce three financial statements on a regular basis. These three financial statements are involved with answering the following questions:

- What cash movements took place?

- How much wealth was generated?

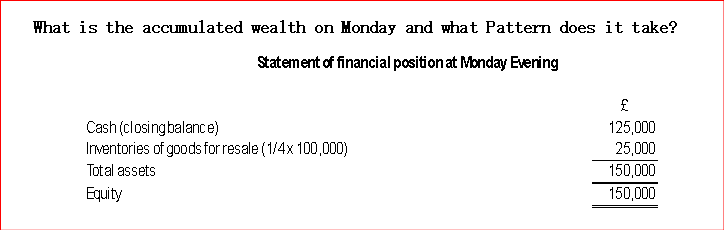

- What is the accumulated wealth at the end of the period and what pattern does it take?

To address the questions above, the financial statements below are required:

- The statement of cash flows;

- The income statement (profit and loss account); and

- The statement of financial position (balance sheet).

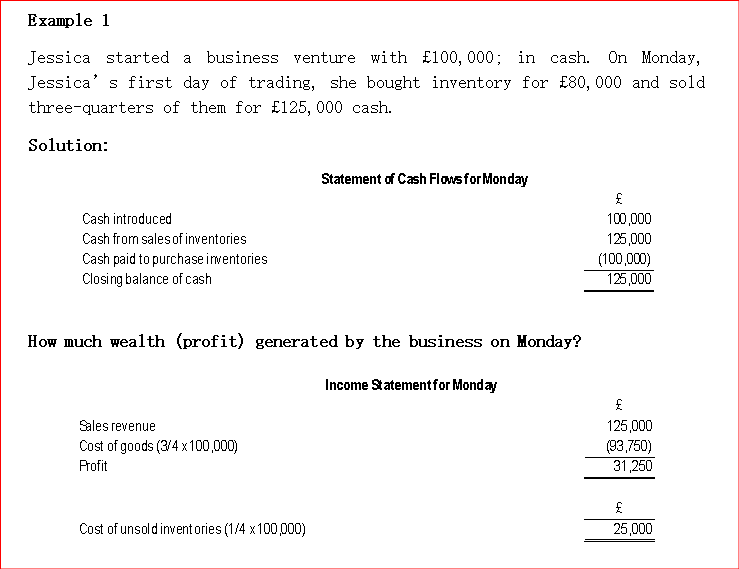

Example 1

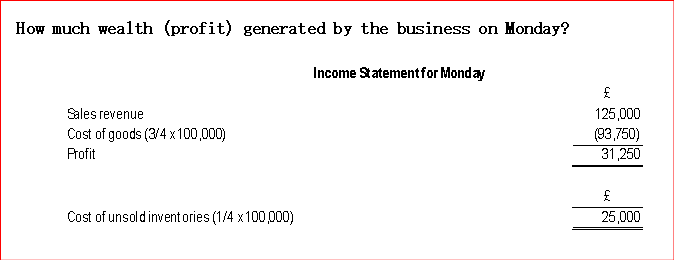

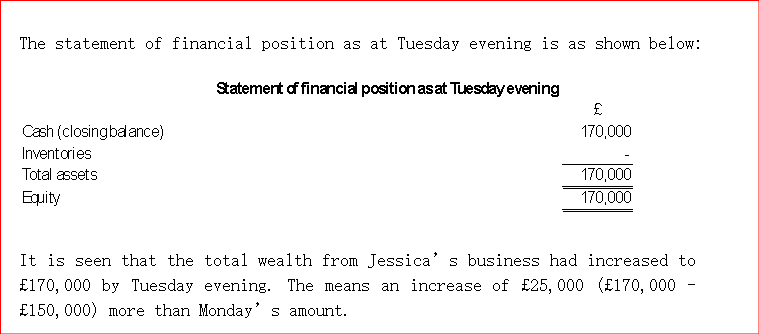

Jessica started a business venture with £100,000; in cash. On Monday, Jessica’s first day of trading, she bought inventory for £80,000 and sold three-quarters of them for £125,000 cash.

Note that the equity represents the business resources and it includes cash and inventories. Thus, the equity on Monday evening was £125,000, which is consists of cash closing balance (£125,000) and a profit of £25,000, totaling £150,000, belonging to the business owner.

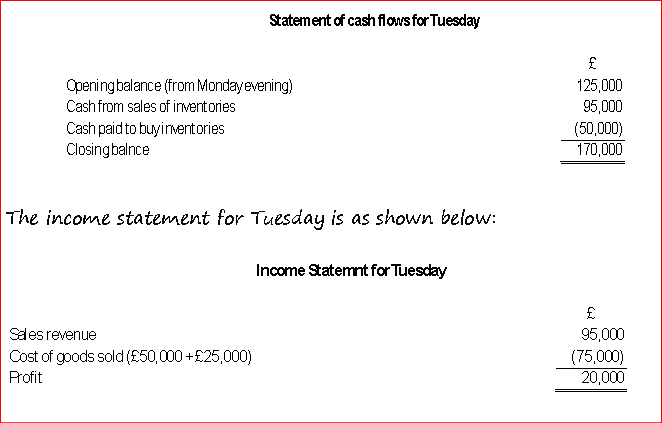

On Tuesday, Jessica purchased more inventories for £50,000 cash. She sold all the new inventories and all the earlier inventories for a total of £95,000.

The statement of cash flows for Tuesday will be as shown below:

Issuing New Shares

Issuing new shares allows a company to raise capital by selling ownership stakes to investors, potentially diluting existing shareholders’ ownership. This constitutes a means to fund growth, investments, or to boost the company’s financial position.

Example 1

Based on prospective outlook, the net assets of company are worth £1.8m. There are currently £1.2m ordinary shares in the company, each with a par value of £1. The company desires to raise an additional £0.7m (700,000 shares) of cash for expansion and has decided to raise it by issuing news shares.

If the shares are issued for £1 each, the total number of shares will be?

£1.2m + £0.7m = £1.9m

The total value will be the value of existing net assets plus the new cash to be injected:

£1.8m + £0.7m = £2.5m

The value of each share after the new issue will be:

£2.5 / £1.9m = £1.316

The current value of each share is:

£1.8m / £1.2m = £1.50

Thus, the original shareholders will lose:

£1.50 – £1.316 = £0.184 a share

And the new shareholders will gain:

£1.316 – £1 = £0.316 a share

The new shareholders will be contented with this outcome; however, the original shareholders will not.

Newly created Subsidiary

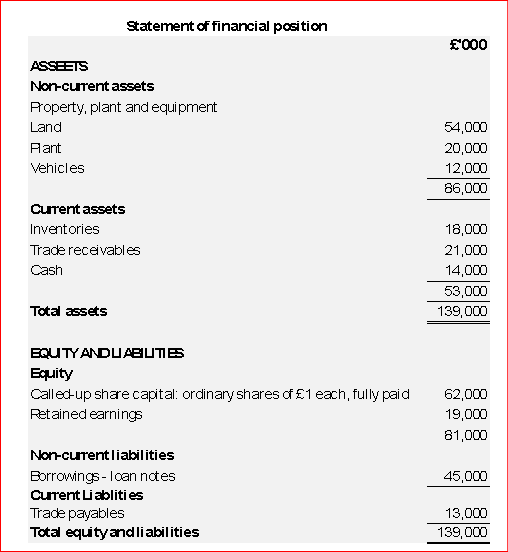

To create a subsidiary, the possible parent probably would simply form a new company in the typical way. The new company would then issue shares to the parent, in exchange for certain asset or assets of the parent. Where the new subsidiary has been established to operate a fully new activity,

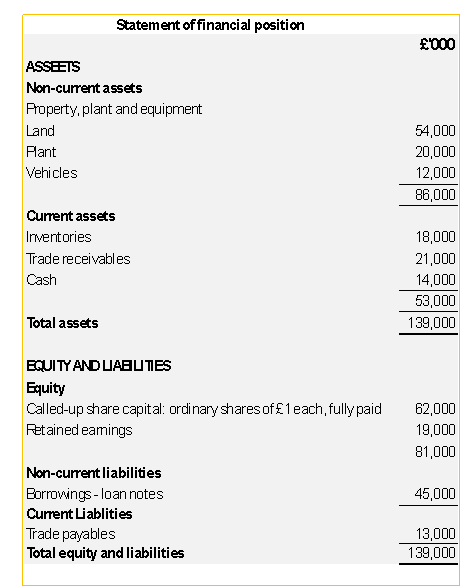

The summarized statement of financial

position of Doxon Co as shown below:

Doxon Co has recently established a new company, Gazin Co, which is to operate task that has been undertaken by industrial textile division of Doxon Co. The assets below are to be transferred to Gazin Co at the values that currently are portrayed in the statement of financial position of Doxon Co:

Doxon Co is to issue £1 ordinary shares at their nominal/par value to Gazin Co in exchange for these assets:

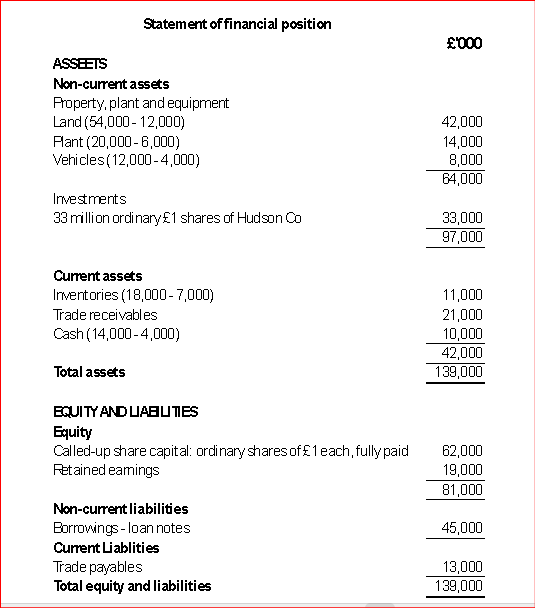

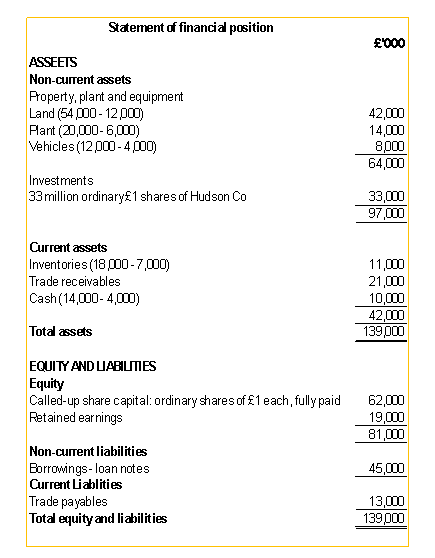

Gazin Co’s statement of financial position shortly after these transfers will be:

Solution:

Doxon Co is to issue £1 ordinary shares at their nominal/par value to Gazin Co in exchange for these assets:

Gazin Co’s statement of financial position shortly after these transfers will be:

Solution:

As seen above, the individual productive assets have been replaced by the asset of shares in Gazin Co.

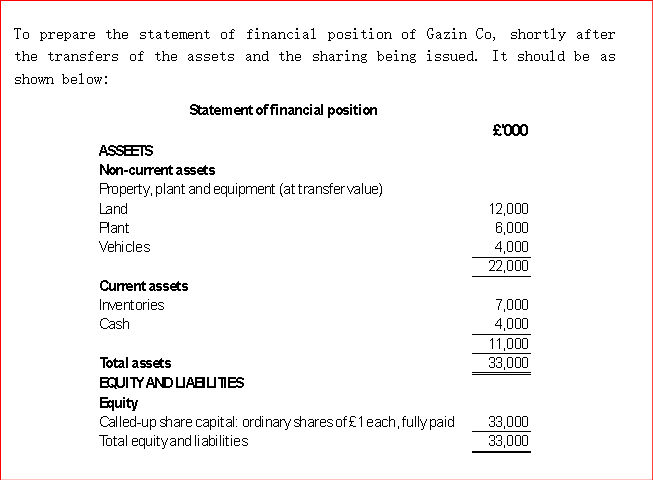

To prepare the statement of financial position of Gazin Co, shortly after the transfers of the assets and the sharing being issued. It should be as shown below:

Revaluation of Assets

Depreciation

- Straight Line Method

By this method, the number of years of use is calculated. The cost is then divided by the number of years, to give the depreciation charge each year.

For example, if a vehicle was purchased for £82,000 and it thought that it would be kept for 5 years and then sell it for £7,000, the depreciation to be charged would be:

Solution:

Cost – Disposal value / Number of years of use

(£82,000 – £7,000) / 5 = £15,000 depreciation each year for five years.

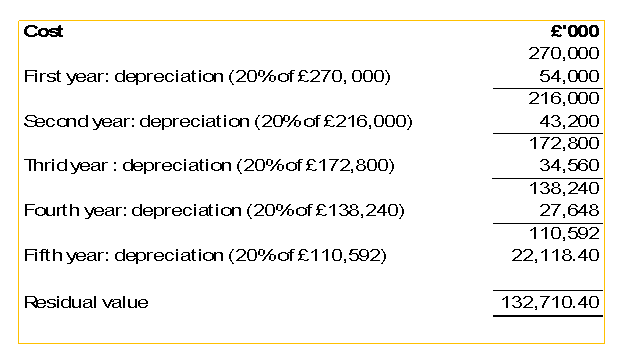

- Reducing Balance Method

For example, if a factory machine was bought for £ 270,000 and the depreciation is to be at 20 percent for 5 years.

Solution:

Double Entry for Depreciation:

- Profit and loss (depreciation expense) account Dr

- Provision for depreciation (accumulated depreciation) account CR

There are more journal entries than the ones above.

Revaluation of Property, Plant and Equipment, and Tangible Fixed Assets, IAS 16 & FRS 15

- Initial Measurement

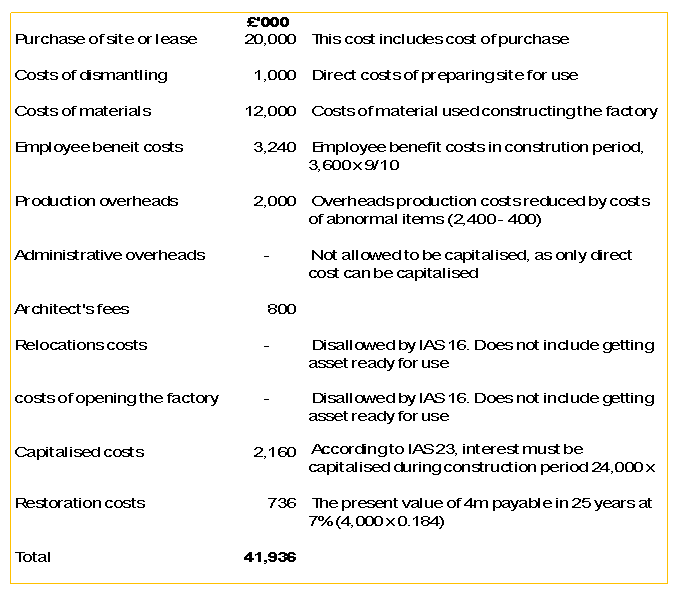

IAS 16 requires that PPE should be measured at cost and the cost of an item of PPE should be recognized if, and only if:

- It is probable that future economic benefits associated with the item will flow to the entity, and

- The cost of the item can be reliably measured.

Direct attributable cost include:

- Purchase price, including import duties and taxes, after deducting trade discounts and rebates.

- Costs employee benefits arising directly from the construction or acquisition of the item of PPE.

- Costs of site preparation.

- Initial delivery and handling costs.

- Costs of installation and assembly costs.

- The cost of testing whether the asset is properly functioning; and

- Professional fees.

- The initial estimate of dismantling and removing the item and restoring the site on which it is located, this cost is recognized as a provision under IAs 37, provisions, Contingent Liabilities and Contingent Assets. The principles of IAS 37 state that the amount can be capitalized, as well as considered as an amount of foreseeable expenditure that is appropriately discounted where the effect is material.

Borrowing costs. IAS 23 requires the inclusion of borrowing costs associated with the financing of a constructed asset.

Examples of costs that are not inclusive of costs of a property, plant, and equipment (PPE):

- Costs of opening a new facility

- Costs of introducing a new product or service (e.g., costs of advertising and promotional activities)

- Costs of conducting or implementing business in a new location or with a customer (e.g., staff training costs), and

- Administration or other general costs.

Example 2

On 1 June 2010, G-Star Co began the construction of a new factory and incurred costs in the year ending 31 July 2011, as stated below:

Note 1: The factory was constructed in the nineth months 29 February 2011. It began operation on 31 March 2011. The costs of employee benefit are for ten months to March 2011.

Note 2: The overheads of production were incurred in the nineth months ended 29 February 2011. This includes an abnormal cost of £400,000 which was incurred owing to the need to repair damage caused by the general heater.

Note 3: G-Star Co obtained a loan of £24m on 1 June 2010 to fund part of the construction of the factory. The loan has a rate of 12% per annum.

Note 4: The factory has an expected useful life of 25years, after which it will be demolished and site restored to its original condition. The restoration will cost a legal fee of £4. A fair discount rate is 7%, which represents a discount factor of 0.184 for the 25-year period.

Solution:

Any cost that is not capitalized as part of setting up the factory will be expensed to the income statement as incurred. Capitalized costs can be accumulated over a period and finally expense to the income statement at end of accounting period.

Example 3

On 1 January 2010, G-Star acquired factory machinery for £300,000. The estimated useful life of the machinery was 15 years; however, its lining requires to be replaced every five years. The cost of the lining on 1 January 2010 was £80,000. The lining was replaced on 1 January 2015 at a cost of £90,000.

Solution:

There are two depreciable components related to the asset:

- The lining component (allocated cost £80,000 with a useful life of five years),

- The remaining cost [allocated cost of £220,000 (£300,000 – £80,000) with a useful life of 15 years].

Thus, the annual depreciation is £30, 666.67 [(£80,000 x 1/5) + (£220,000 x 1/15)]. On 31 December 2014, the lining component has a carrying value of zero.

From 2015:

The £90,000 expended on the new lining is treated as the replacement of a different component of an asset and capitalizes a part of PPE. The annual depreciation charge for the machinery is now £32,666.67 [(£90,000 x 1/5) + (£220,000 x 1/15)].

Revaluation of Property, Plant and Equipment (IAS 16)

IAS 16 permits entities the choice of two valuation models for PPE, namely the cost model or the revaluation model.

- The cost model is treated as asset cost less accumulated depreciation and any accumulated impairment losses.

- The revaluation model is treated as asset at its fair value at the revaluation date less subsequent depreciation and subsequent impairment losses).

- Revaluation Gain

Revaluation gain is an increase in asset value recorded when it is revalued to their fair value, rather than their original costs. This gain is typically recognized in the ‘other comprehensive income’ and accumulated in equity under a ‘revaluation surplus’ heading. However, it can also be recognized in the statement of profit or loss if it reverses a previous revaluation loss recognized in the same statement.

Journal entry for revaluation gain:

- Revaluation surplus account Cr

- Asset account Dr

Example 4

A property was acquired on 1 January 2005 for £4m (estimated depreciable amount £2m -useful economic life 50 years). Annual depreciation of £40,000 was charged from 2005 to 2009. On 1 January 2010 the carrying value of the property was £3.8m. The property was revalued to £5.6m on 1 January 2010 (estimated depreciable amount £2.7m – the estimated useful economic value life was unchanged).

Solution:

The revaluation surplus of £5.6 – £3.8 = £1.8 is recognized in the statement of change in equity by crediting a revaluation reserve account and debiting property account. The depreciable amount of property is now £2.7m and the remaining estimated useful economic life is 45 years (50 years from 1 January 2005). Thus, the depreciation charge from 2010 onwards would be £60,000 (2.7m x 1/45).

A revaluation often increases the annual depreciation charge in the income statement. In the example above, the annual increase is £20,000 (£60,000 – £40,000).

The IAS 16 permits (but does not require) entities to make a transfer of ‘excess depreciation’ from the revaluation reserve directly to retained earnings.

- Revaluation loss

A revaluation loss is referred to as the decrease in value of an asset, namely property, plant and equipment, when its fair value is lower than its carrying value (book value) after revaluation. This revaluation loss is recognized as an expense in the income statement, and it is also recognized in equity and deducted from a previous revaluation surplus.

Example 5

If the property referred to in example 1 was revalued on 31 December 2011. Its fair value had fallen to £3m.

Solution:

The carrying value of the property on 31 December 2011 would have been £5.36m (£5.6m – 4 x £60,000). This means that the revaluation deficit is £2.36m (£5.36m – £3m).

If the transfer of excess depreciation (see above) is not made, then the balance in the revaluation reserve relating to this asset £1.8 (see example 1). Thus, £1.8 is deducted from equity and £560,000 (£2.36 – £1.8) is charged to the income statement.

If the transfer of excess depreciation is made, then the balance on the revaluation reserve on 31 December 2011 is £1.72m (£1.8m – 4 x £20,000). Thus, £1.72m is deducted from equity and £640 (£2.36 – £1.72) is charged to the income statement.

Derecognition of PPE, The IAS 16

The PPE should be derecognized; that is, removed/scrapped from PPE, either on disposal or when no future economic benefit is expected from the asset. A gain or loss is recognized as the differential between the disposal value and the carrying value of the asse (applying the cost or revaluation model) at the date of disposal. Consequently, the net gain is transferred to income statement as “Other revenue or Expense”.

Disposal of Assets, IFRS 5

Under IFRS 5, a non-current asset or a disposal group is classified as “held for sale” when its carrying amount will be recovered basically through a sale instead of continuing use. A disposal group is a group of assets, possibly with related liabilities, that an entity intends to dispose of in a single transaction.

The Journal Entry for Disposable Assets:

- Gain on Disposal:

- If the selling price exceeds the asset’s book value, the difference is a gain.

- The journal entry will include:

- Debit: Cash (amount received from the sale)

- Debit: Accumulated Depreciation (to remove the asset’s accumulated depreciation)

- Credit: Asset (to remove the asset’s original cost)

- Credit: Gain on Disposal (for the difference between the selling price and book value)

- If the selling price is less than the asset’s book value, the difference is a loss.

- The journal entry will include:

- Debit: Cash (for the amount received from the sale)

- Debit: Accumulated Depreciation (to remove the asset’s accumulated depreciation)

- Debit: Loss on Disposal (for the difference between the selling price and book value)

- Credit: Asset (to remove the asset’s original cost)

Example 6

An asset has a carrying value of £900,000. It is classified as held for sale on 30 September 2011. At that date its fair value minus costs to sell is estimated at £950,000. The asset was sold for £955,000 on 30 November 2011. The year end of the entity is 31 December 2011.

Solution:

The classification as held for sale, and subsequent disposal, be treated as follows:

- On 30 September 2011, the asset would be treated as: its fair value less costs to sell £950,000 and an impairment loss of £50,000 is recognised. This amount would be removed from non-current assets and presented in “non-current assets held for sale”. On 30 November 2011 a profit on sale of £5,000 would be recognised.

- On 30 September 2011, the asset would be transferred to non-current assets held for sale at its existing carrying value of £900,000. When the asset is sold on 30 November 2011, a profit on sale of £55,000 would be recognised.

Bad Debts and Provision of Doubtful Debt

Bad Debts:

If a company realizes that it is impossible to collect a debt, then that debt should be written off as a bad debt. This could occur if the debtor encounters a loss in the business, or perhaps even gone bankrupt and is thus unable to pay the debt. Therefore, a bad debt becomes an expense on the company that is owed the money.

Example:

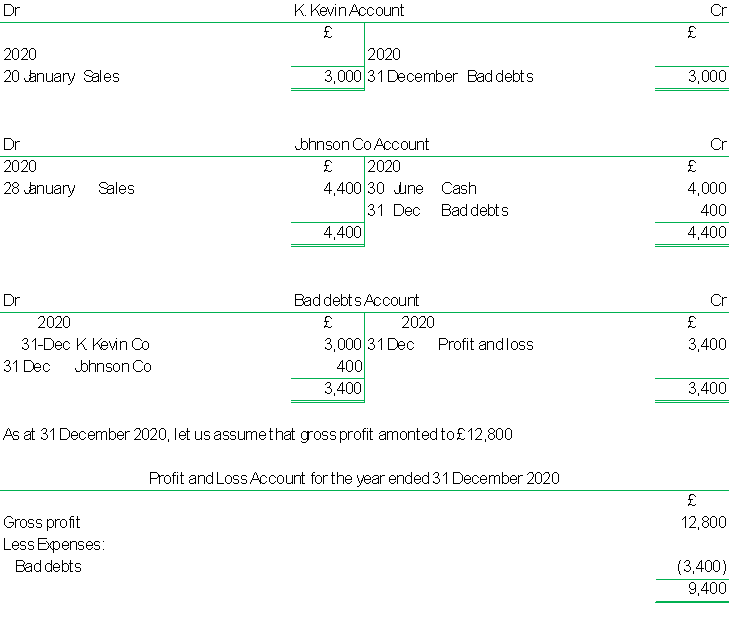

Dadin Co sold £3,000 goods to K. Kevin Co on 20 January 2020, and K. Kevin Co became bankrupt.

On 28 January 2020, Dadin Co sold £4,400 goods to Johnson Co. Johnson managed to pay £4000 on 30 June 2020, but it became obvious that he would never be able to pay the final £400.

At 31 December 2020, when Dadin Co is drawing up final accounts, it decided to write these off as bad debts. The account entries are shown below:

Issuing New Shares

Issuing new shares allows a company to raise capital by selling ownership stakes to investors, potentially diluting existing shareholders’ ownership. This constitutes a means to fund growth, investments, or to boost the company’s financial position.

Example 1

Based on prospective outlook, the net assets of company are worth £1.8m. There are currently £1.2m ordinary shares in the company, each with a par value of £1. The company desires to raise an additional £0.7m (700,000 shares) of cash for expansion and has decided to raise it by issuing news shares.

If the shares are issued for £1 each, the total number of shares will be?

£1.2m + £0.7m = £1.9m

The total value will be the value of existing net assets plus the new cash to be injected:

£1.8m + £0.7m = £2.5m

The value of each share after the new issue will be:

£2.5 / £1.9m = £1.316

The current value of each share is:

£1.8m / £1.2m = £1.50

Thus, the original shareholders will lose:

£1.50 – £1.316 = £0.184 a share

And the new shareholders will gain:

£1.316 – £1 = £0.316 a share

The new shareholders will be contented with this outcome; however, the original shareholders will not.

Newly Created Subsidiary

To create a subsidiary, the possible parent probably would simply form a new company in the typical way. The new company would then issue shares to the parent, in exchange for certain asset or assets of the parent. Where the new subsidiary has been established to operate a fully new activity,

The summarized statement of financial position of Doxon Co as shown below:

Doxon Co is to issue £1 ordinary shares at their nominal/par value to Gazin Co in exchange for these assets:

Gazin Co’s statement of financial position shortly after these transfers will be:

Solution:

As seen above, the individual productive assets have been replaced by the asset of shares in Gazin Co.

To prepare the statement of financial position of Gazin Co, shortly after the transfers of the assets and the sharing being issued. It should be as shown below: