Business Acquisition Accounting

1.1. Method 1: Acquisition of Net Assets

The acquisition of net assets, in the context of business combinations or mergers and acquisitions (M&A), is referred to as the process of a company acquiring the net assets (assets minus liabilities) of the acquired company. The net assets are normally valued at fair value, and the difference between the purchase price and the fair value of the net assets can result in goodwill or a bargain purchase.

1.2. Method 2: Acquisition of Shares

A share acquisition (a share purchase or share sale), is a transaction where one entity (the buyer) purchases shares in another company (the target) to gain ownership or control that typically determined by the percentage of ownership.

1.3. Business Combination, IFRS 3

IFRS 3, “Business Combinations,” mandates the accounting treatment for acquisitions of businesses. It outlines how an acquirer recognizes and measures assets, liabilities, and goodwill in a business combination, using the acquisition methods. Fundamentally, it provides a framework for accounting for takeovers, mergers, and other transactions where one entity gains control of another.

IFRS 3 establishes principles and requirements for how an acquirer in a business combination:

- recognises and measures in its financial statements the assets and liabilities acquired, and any interest in the acquiree held by other parties;

- recognises and measures the goodwill acquired in the business combination or a gain from a bargain purchase; and

- determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects of the business combination.

1.3.1. Purchase Consideration

Purchase consideration refers to the aggregate value of everything an acquiring company gives to a selling company in exchange for the assets or business being acquired. It is importantly the price the buyer pays to take ownership of seller’s assets or business. This consideration can be cash, shares of the acquiring company, deferred consideration (valued at present value of the future payment), or a combination of these.

Example:

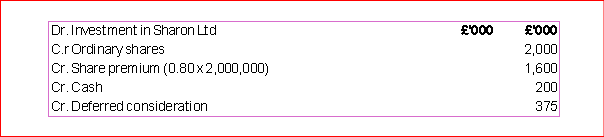

Jack Plc acquired 90% of the ordinary shares of Sharon Ltd on 1 October 2010 for the following considerations:

- the issue of two million £1 ordinary shares at market value £1.80;

- an immediate cash payment of £200,000; and

- a cash payment of £500,000, three years after the date of the acquisition.

Jack Plc can borrow funds at 10%.

Journal entry to record the purchase consideration in the financial statements of Jack plc:

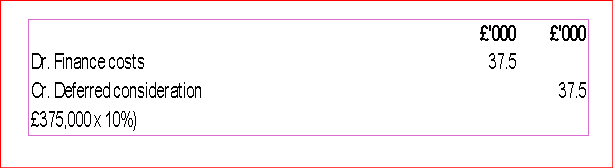

The deferred consideration is estimated at present value, at a discount factor of 0.7513.

The total deferred consideration discount of £125,000 (500,000 – 375,000) is unwound over three years and accounted for in the consolidated financial statements in the year ended 30 September 2011 as shown below:

Accounting for Investments

The accounting for investments involves tracking, measuring, and reporting and compliance (GAAP & IFRS) on the value of investments to understand profit and loss, tax reporting, risk and the overall effect on an organisation’s financial performance. Investment measurements can be done through equity method (e.g., 20%-50% ownership), fair value method (for trading or available for sale), and cost method (non-controlling stakes, less than 20% ownership).

2.1. Subsidiary

IFRS 10 Consolidated Financial Statements defines a subsidiary as an entity that is controlled by another entity (the parent company).

Example 1:

Johson Co acquires more than 50% of the voting rights of another entity (Judin Co) and decision-making is resolved by voting rights.

On 1 September 2005, Johnson Co acquired £2.4m of the ordinary shares of Judin Co. At that date Judin Co had £3m ordinary shares in issue. Thus, Johnson Co has acquired an 80% holding (£2.4M/£3m = 80%).

2.2. Associate

IAS 28 Investments in Associates and Joint Ventures defines an associate as an entity over which the investor has significant influence. The significant influence is the “power to participate in the financial and operating policy decisions of the investee but is not control of those policies.

On 1 January 2005, Akin Ltd acquired 80m of the 200m ordinary shares in issue by Orange Ltd. Akin Ltd has now acquired an associate, because it has acquired between 20% and 50% of the voting right shares.

2.3. Joint Venture

IAS 28 Investment in Associate and Joint Ventures defines a joint venture as a “joint agreement whereby the parties that have joint control of the agreement have rights to the net assets of the agreement.

On 1 February 2005, Soso Ltd and Asun Ltd, entities that are related, acquire 50% each of the ordinary shares of Gogo Ltd and will jointly control the agreement.

2.4. Trade or Simple Investment

A trade or investment occurs where an investor acquires less than 20% of the voting rights of the investee and the investment can be considered to bring about a significant influence.

Accounting Standards for trade investment are the IFRS 9 ‘Financial Instruments’ and the IAS 39 ‘Financial Instruments Recognition and Measurement’. The standard encompasses requisites for recognition and measurement, impairment, derecognition, and general hedging accounting.

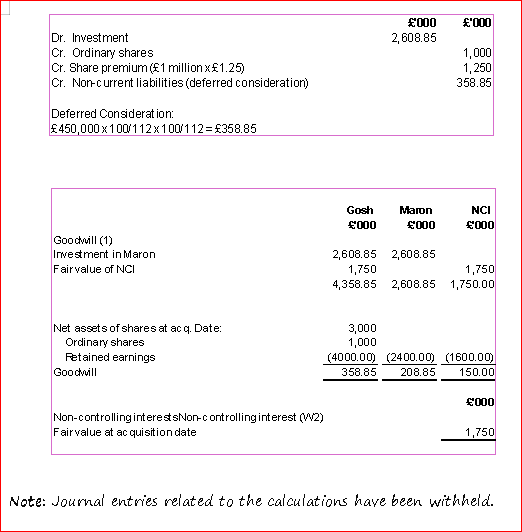

Goodwill and Non-controlling Interests

Gosh Ltd acquired 65% of the ordinary shares of Maron Ltd on 1 October 2021 when the issued share capital of Maron Ltd was £3 million and its retained earnings £1 million. The consideration is as follows:

- the issue of one million ordinary £1 shares in Gosh Ltd at market value £2.25;

- a cash payment of £450,000 on 1 October 2023.

Gosh Ltd can borrow funds at 12%.

The non-controlling interests in the net assets of Maron Ltd as at 1 October 2021 is valued at £1,750,000.

Solutions.

Journal entry to record purchase consideration: