FINANCIAL REGULATIONS

Financial regulation comprises the laws, rules, and guidelines that supervise the operations of financial institutions, markets, and transactions. These regulations are vital for maintaining stability, protecting consumers and investors, ensuring equitable competition, and fostering transparency and competition in financial institutions and markets.

The Basel Accords are a set of international banking regulations stipulated by the Basel Committee on Banking Supervision (BCBS).

- Basel I (1998):Set standards for minimum amount of capital banks must hold to make up for potential losses occurring from credit, market, and operational risks.

- Basel II (2004):Fine-tuned risk management and sensitivity, introducing operational and market risks, and incorporated a three-pillar framework: minimum capital requirements, supervisory review, and market discipline.

- Basel III (2010):Enhanced capital requirements in reaction to the 2008 financial crisis, incorporated liquidity and leverage ratios, and focussed on fostering the quality of capital and improving risk coverage.

Prudential Regulatory Reporting

In the perspective of financial regulation, prudential regulatory reporting is the process by which financial, specifically banks and insurers, submit elaborated financial data to regulatory authorities (e.g., Prudential Regulatory Authority, UK) regarding their financial health, practices of risk management, and operational activities. By submitting this report, financial institutions demonstrate their compliance with the rules entrenched to guarantee financial stability and prevention of systemic risk. In essence, it is a mechanism through which institutions demonstrate that they are prudently managing risk and have adequate resources to meet their obligations.

Prudential Regulatory Authority (PRA 110)

PRA 110 is referred to as a regulatory reporting requirement brought about by the Prudential Regulation Authority (PRA) in the UK for regulating financial institutions, such as banks, building societies, PRA-designated companies, and UK branches of European Economic Area (EEA) companies. This reporting requirement, established 2019, aims to render the regulator a more granular and profound view of short-term liquidity risks encountered by financial institutions.

- Short-term Liquidity

PRA110 particularly targets liquidity risks within a short-term timeline, usually less than 30 days, elaborating the extent of the Liquidity Coverage Ratio (LCR) by giving a more elaborated day-to-day analysis for the initial months.

- Evaluation of Risks

The report/return helps the PRA assess several core perspectives of liquidity risk. Key components are:

- Balance Sheet Data as an Input

PRA 110 statutorily requires companies to report cash movements of contractual obligations and maturities (inflows and outflows) derived from both on-balance sheet entries (e.g., loans and deposits) and off-balance sheet exposures (e.g., contingent liabilities, unused credit lines, and guarantees).

- Counterbalancing Capacity (CBC)

The aspect constitutes the stock of unencumbered or liability-free assets or other funding sources available for a company to cover potential contractual gaps, which are directly associated with assets contained on the balance sheet.

- Memorandum Entries

The aspect joins existing liquidity report requirements with new data points, encompassing details on derivatives and their connected associated margins, which are always related to off-balance sheet entries.

- Essence of Data Quality

The consistency and accuracy of data obtained from balance sheet and related off-balance sheet entries are germane for an error-free PRA 110 return/report.

- Data Requirements and Reporting Frequency

PRA 110 return is complex and requires essential data (including due diligence), typically with short processing and returning times. Larger companies (holding assets of around £25 billion (€30 billion) or above) must complete the return weekly, while smaller companies are required to do so monthly. In circumstances of heightened liquidity distress, the reporting frequency for some companies could be returned daily.

- Cash Flow Mismatch

In the perspective of PRA110, a cash flow mismatch represents the difference between a firm’s cash inflows and outflows over stipulated time horizons, specifically under stress scenarios. The PRA110 monitors short-term liquidity risks and potential stress within financial institutions, such as banks and building societies.

Specifically, a cash flow mismatch indicates whether a firm has adequate cash flow monetized liquid assets and other inflows to cover its outflows (daily basis), under stressed scenarios. The PRA110 return reveals situations where:

- A bank may hold inadequate High Quality Liquid Assets (HQLA) to meet topmost liquidity needs within a 30-day period.

- A bank may be unable to readily convert its non-cash HQLA into cash quickly enough to cover cumulative or culminating net outflows under a stress situation, based on the framework of Liquidity Coverage Ratio (LCR).

- Helps to identify potential weaknesses and vulnerabilities in liquidity risk management, including to monitor intraday risks and timing mismatches.

- Complexities and Challenges: Owing to the comprehensive nature and tight deadlines, executing and managing the PRA110 return can pose challenges for financial institutions. Efficient management of data, viable processes, and proficient resources are significant to ensure compliance.

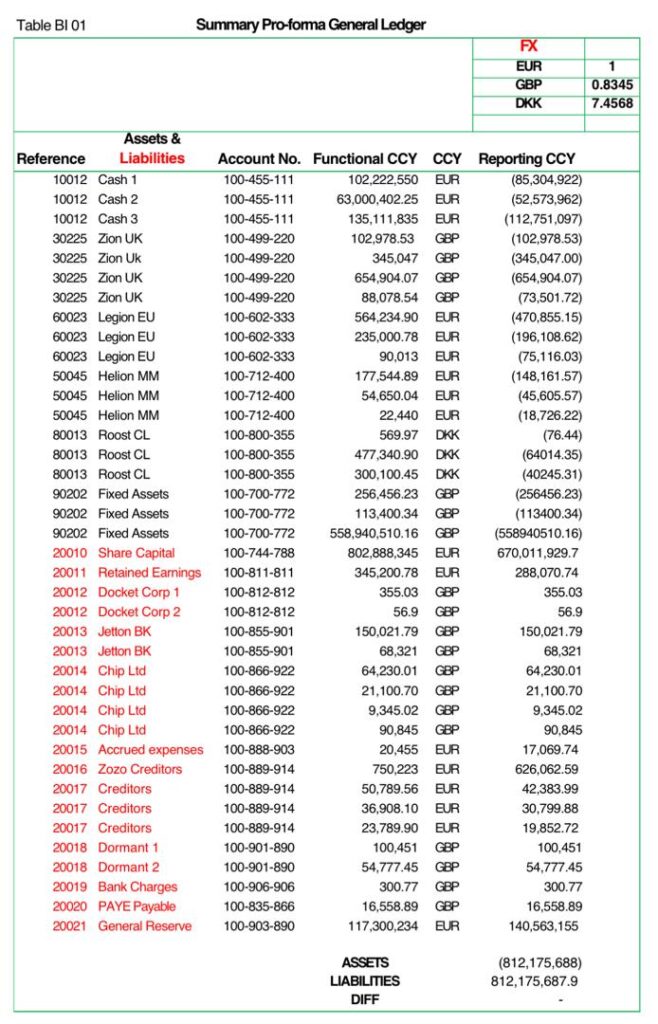

Table BI 01 above portrays an exemplar pro-forma general ledger with which financial regulatory return can be computed.

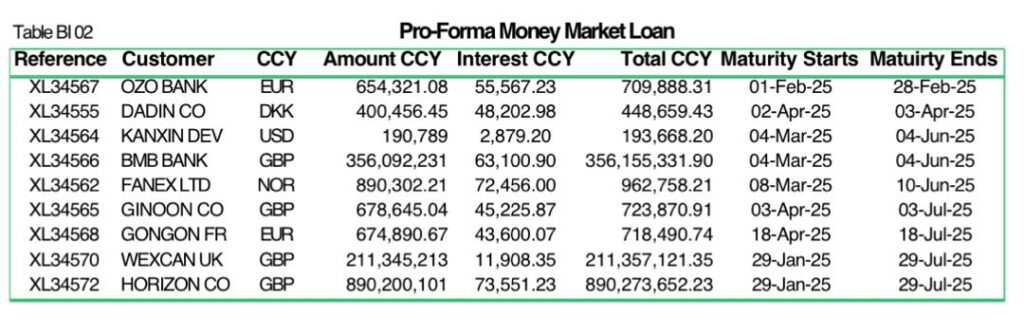

Table BI 02 depicts an exemplar pro-forma data of money-market deals with which financial regulatory return is prepared, alongside the entries of general ledger. However, both Table BI 01 and Table BI 02 are nowhere near big-data spreadsheets of an average firm’s financial regulatory return, which are complex, high-level of expertise in financial modelling and analysis, and due diligence.

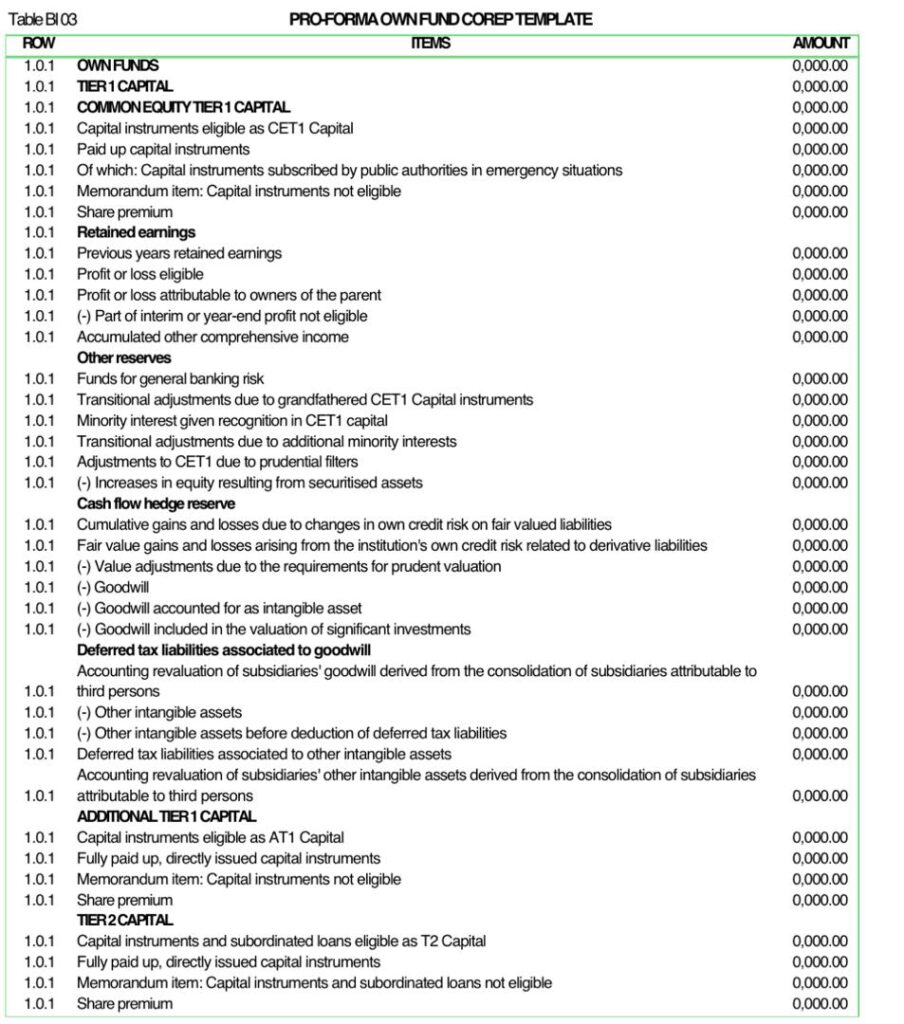

Common Reporting (COREP)

Common Reporting represents a standardized regulatory reporting framework set up by the European Banking Authority (EBA). It mandates credit institutions and investment companies to report on their capital adequacy, risk exposures, such as credit, market, operational risk, and own funds, making sure that consistent and harmonized reporting across the European Union.

- Purpose

COREP focuses to enhances transparency and consistency in regulatory reporting by standardizing the composition or format and components of reports submitted to supervisory authorities.

- Scope

It comprises diverse sections of a firm’s financial health and risk profile, encompassing:

- Capital Adequacy:Guaranteeing firms keep adequate capital to cover potential losses.

- Credit Risk:Evaluating the risk of borrowers defaulting on their obligations.

- Market Risk:Assessing the potential influence of adverse market behaviour on a firm’s financial position.

- Operational Risk:assessing the risk of losses arising from insufficient or failed internal procedures, people, and systems, or from external activities.

- Own Funds:Reporting the various sections of a firm’s capital base.

- Capital Adequacy Ratios:Computing and reporting the ratios that show a firm’s capital strength in connection with its risk-weighted assets.

- Harmonization

COREP replaces different national reporting requirements with a single, harmonized framework, facilitating simpler comparison and analysis of data across various institutions and jurisdictions.

- Implementation

COREP is executed through a set of reporting templates and technical standards, which are regularly updated by the EBA. These templates are used to collect and submit data to the essential supervisory authorities.

- Relationship with FINREP

COREP is often mentioned alongside FINREP (Financial Reporting), which is another EBA reporting framework centred on financial reporting (balance sheet, income statement, etc.). In conjunction, COREP and FINREP provide an all-encompassing and well-detailed view of a firm’s financials and risk position.

COREP Reporting Templates (EBA)

The EBA regularly updates the COREP reporting framework 2.7, along with templates via Technical Standards (ITS), for credit institutions and investment companies to report their solvency ratio to supervisory authorities under the Capital Requirements Directive (CRD) III or IFRS 9.

Key Features of COREP Reporting Templates:

- Scope:COREP contains reporting on a firm’s own funds and capital requirements, including sections like Capital Adequacy, Group Solvency, Credit Risk, Operational Risk, Market Risk, Large Exposures, and Leverage.

- Harmonization:The EBA focuses on a high level of harmonization and convergence of supervisory reporting requirements across the EU through the COREP stipulated framework.

- Formats:Reporting is typically done using XBRL instance files, which are a standardized technical implementation of the Data Point Model (DPM).

- Accessibility:The EBA publishes the reporting requirements, as well as the ITS on supervisory reporting and the XBRL taxonomies, on its website.

- Updates:The EBA periodically updates the XBRL taxonomy and DPM to manifest alterations in regulations and reporting requirements.

Ultimately, in each EU member state, competent authorities may provide more guidance and assistance concerning COREP reporting and the utilization of the EBA’s templates and taxonomy.

FINREP Reporting

FINREP (Financial Reporting) is a standardized reporting framework, first developed by the European Banking Authority (EBA) to harmonize financial reporting for banks and financial institutions across the European Union and European Economic Area (EEA), then espoused by national authorities, such as the UK through the Prudential Regulatory Authority (PRA)

Key Features of FINREP Reporting:

- Scope and purpose

FINREP obliges financial institutions listed on a stock exchange or preparing financial statements based on IFRS/GAAP (depending on the jurisdiction) to report comprehensive financial data. The major objectives are to give regulators a full awareness of an institution’s financial health and performance for improved supervision, and to scrutinize the financial stability of the banking system.

- Reporting requirements

FINREP sets out the required financial information, as well as details on balance sheet items, income, expenses, and equity. Reports are normally submitted quarterly and use standardized data formats and descriptions for consistency.

- FINREP templates and instructions

The framework comprises of many templates and information fields that institutions must complete. Instructions for these templates define the rules for recognition, offsetting, and valuation premised on the relevant accounting framework (IFRS or national GAAP). FINREP templates are accessed through sources, such as the European Banking Authority (EBA) website.

- Taxonomy and validation rules

A Data Point Model (DPM) is used to represent the data structure and validation rules for accurate and consistent reporting. This DPM generates the XBRL taxonomy for standardized data sharing. Validation rules, periodically released by the EBA, guarantee data accuracy and consistency between frameworks, namely FINREP and COREP.

- Key actions for FINREP reporting

Institutions are necessitated to comprehend the latest FINREP requirements, pinpoint and source the relevant data, and well-organized reporting processes. Complying with deadlines and reconciling accounting and prudential consolidation groups are also vital steps.

FINREP focuses on developing a consistent and transparent financial reporting environment, permitting regulators to evaluate the financial health of institutions and implement supervisory actions.

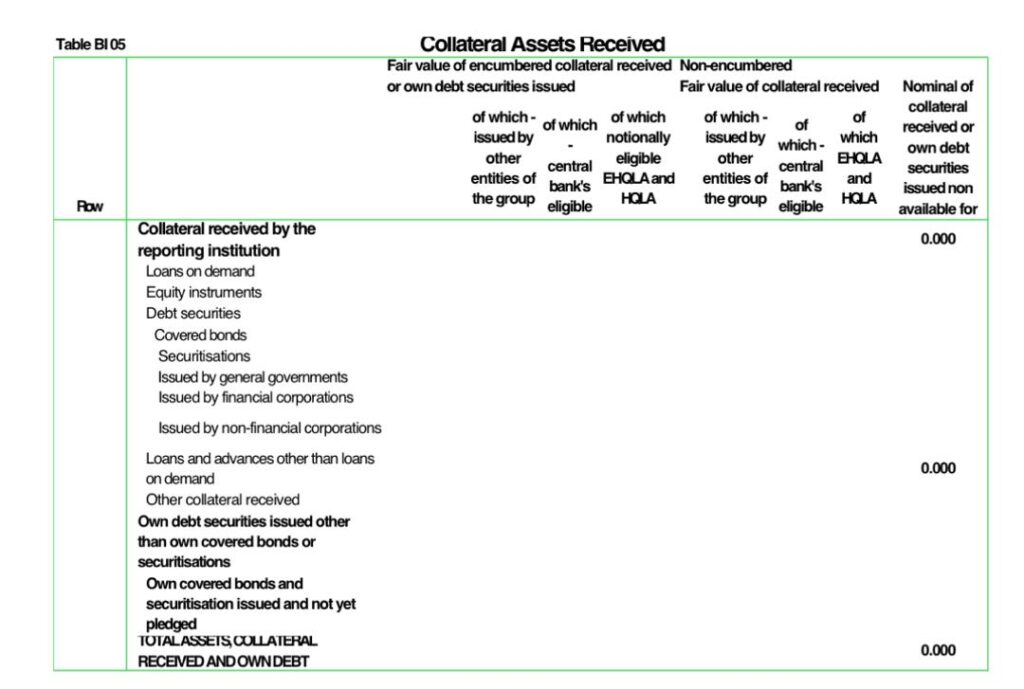

Asset Encumbrance

Asset encumbrance reporting is a process that, under regulation (EU) No 575/2013 (CRR), mandates financial institutions to reveal information about their encumbered assets (i.e., pledged assets) to supervisory authorities. This reporting is planned to provide a comprehensive record of an institution’s risk description and to foster financial stability by allowing regulators to evaluate potential susceptibilities associated with asset encumbrance.

Key Features of asset encumbrance reporting:

- Meaning of Encumbered Assets

Encumbered assets are those that are subject to legal, regulatory, contractual, or other restrictions that limit their use, sale, or transfer. These restrictions can occur from different sources, namely secured financing transactions, collateral deals, financial guarantees, including central bank facilities.

- Reporting Requirements

Institutions are mandated to report on the value and structure of their encumbered assets, in addition to the natures of encumbrances influencing those assets. The reporting frequency and specific data requirements as stipulated in regulations, such as the European Banking Authority’s Implementing Technical Standards.

- Purpose of Reporting

The fundamental goal of asset encumbrance reporting is to improve transparency and comparability of financial risk profiles of institutions. This helps supervisors to identify potential risks associated with to asset encumbrance, such as funding risk and liquidity risk, and adopt appropriate supervisory measures.

- Frequency

Reporting periods range from a quarterly, annual, to semi-annual basis, depending on the specific requirements and size of the institutions.

- Supervisory Scrutiny

Supervisory authorities utilize the reported financial data to scrutinise the level of asset encumbrance within the financial system and to evaluate the potential effect on financial stability. This assists them to identify institutions that are vulnerable to high levels of encumbrance and to make sure that they have adequate unencumbered assets to meet their obligations.

- Harmonization and Convergence

The European Banking Authority (EBA) plays a core role in harmonizing asset encumbrance reporting across the European Union. The EBA improve and sustains standardized reporting templates and instructions to guarantee consistency and comparability of data across various institutions and jurisdictions.

Examples of Encumbered Assets:

- Assets used as collateral for secured financing transactions, such as securities lending, repurchase agreements.

- Assets pledged as collateral for derivative transactions.

- Assets used as collateral for central bank funding.

- Assets in cover pools used for covered bond issuance.

Effect of Asset Encumbrance:

- Liquidity Risk

High levels of encumbered assets can mitigate a bank’s capability to evaluate funding in times of distress.

- Funding Risk

If a bank depends hugely on encumbered assets for funding, it may encounter hurdles in refinancing its liabilities.

- Losses for Creditors

In a distressed scenario, unsecured creditors may encounter higher losses if a bank’s assets are hugely encumbered.

- Reduced Financial Stability

High levels of asset encumbrance can bring forth financial uncertainty by rising the risk of systemic risk and contagion.